ETFsInvesting

XEQT vs VFV: Which ETF Should Canadians Buy in 2026?

XEQT vs VFV for Canadian investors in 2026. Which ETF belongs in your TFSA or RRSP, how they differ, and the simple answer for long term investors.

By Ali Hamie·

Category

The Canadian financial system is confusing by design. We un-confuse it.

XEQT vs VFV for Canadian investors in 2026. Which ETF belongs in your TFSA or RRSP, how they differ, and the simple answer for long term investors.

Once your TFSA is maxed, your next move depends first on your tax bracket, then your home plans, FHSA eligibility, RRSP room, pension, and taxable account needs.

Investing feels scary at first, but beginners do not need predictions, charts, or perfect timing. They need diversification, consistency, and time.

Canada just launched the Canada Strong Fund, its first sovereign wealth fund. Here is what is confirmed, what is still unknown, and whether regular Canadians should invest when the retail product arrives.

Your emergency fund should not sit in chequing or in a fake high-interest account at a big bank. Here is where to keep it in Canada, and why a separate online savings account usually wins.

FHSA withdrawal rules in Canada explained: qualifying withdrawals, RC725 form, tax-free rules, taxable withdrawals, and what happens if you do not buy a home.

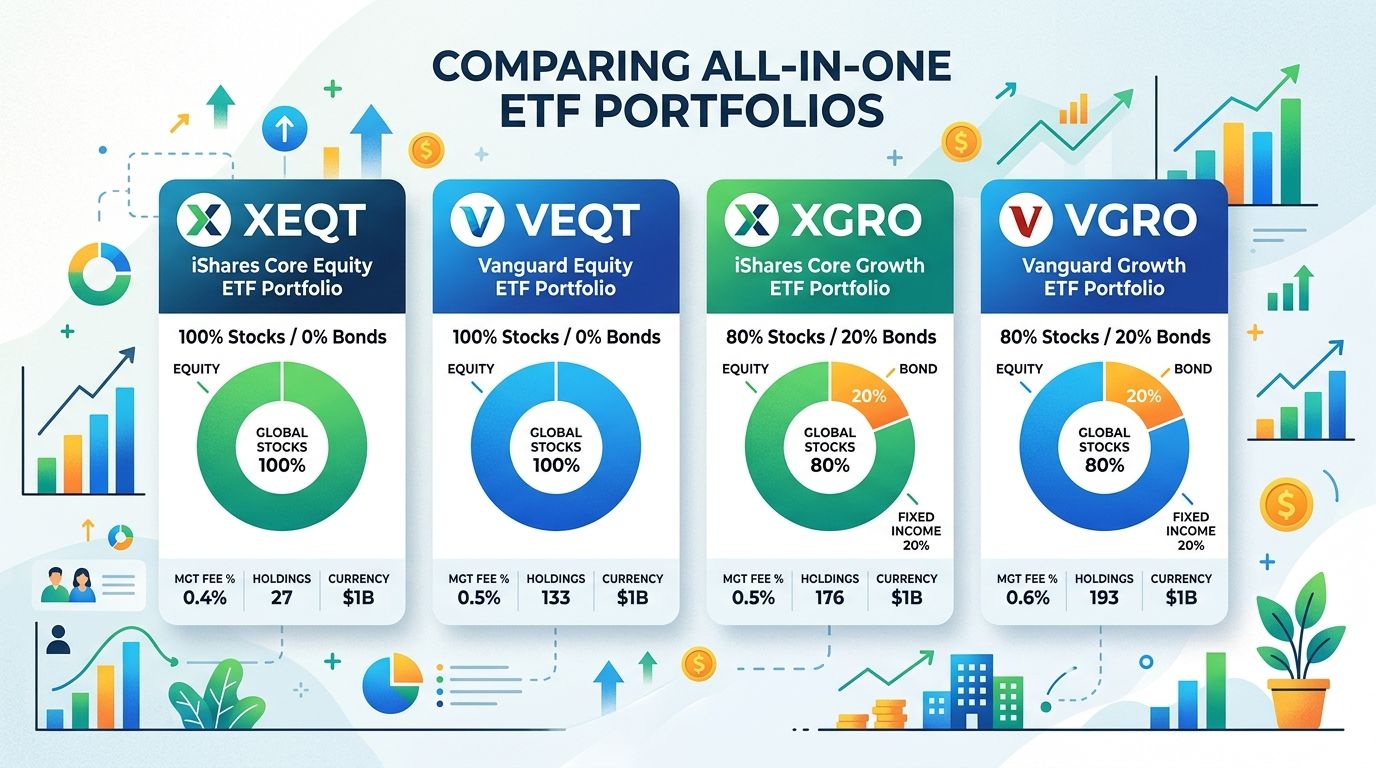

VEQT, XEQT, VGRO, or XGRO? Compare risk, stock and bond mix, fees, and the investor each all in one ETF fits best.

Tax refund sitting in your account? Here is exactly what to do with it: pay off debt first, top up your emergency fund, then TFSA, RRSP, or FHSA depending on your situation.

Capital gains tax in Canada explained: how the 50% inclusion rate works, what triggers tax, capital losses, and legal ways to pay less. Updated for 2026.

The RRSP Home Buyers' Plan lets you pull up to $60,000 tax-free from your RRSP for a first home purchase, with 15 years to pay it back. Here is how to use it properly.

Both platforms now offer free trades. But Wealthsimple charges 1.5% every time money crosses the CAD/USD border — on the buy and the sell. Here's what that actually costs you.

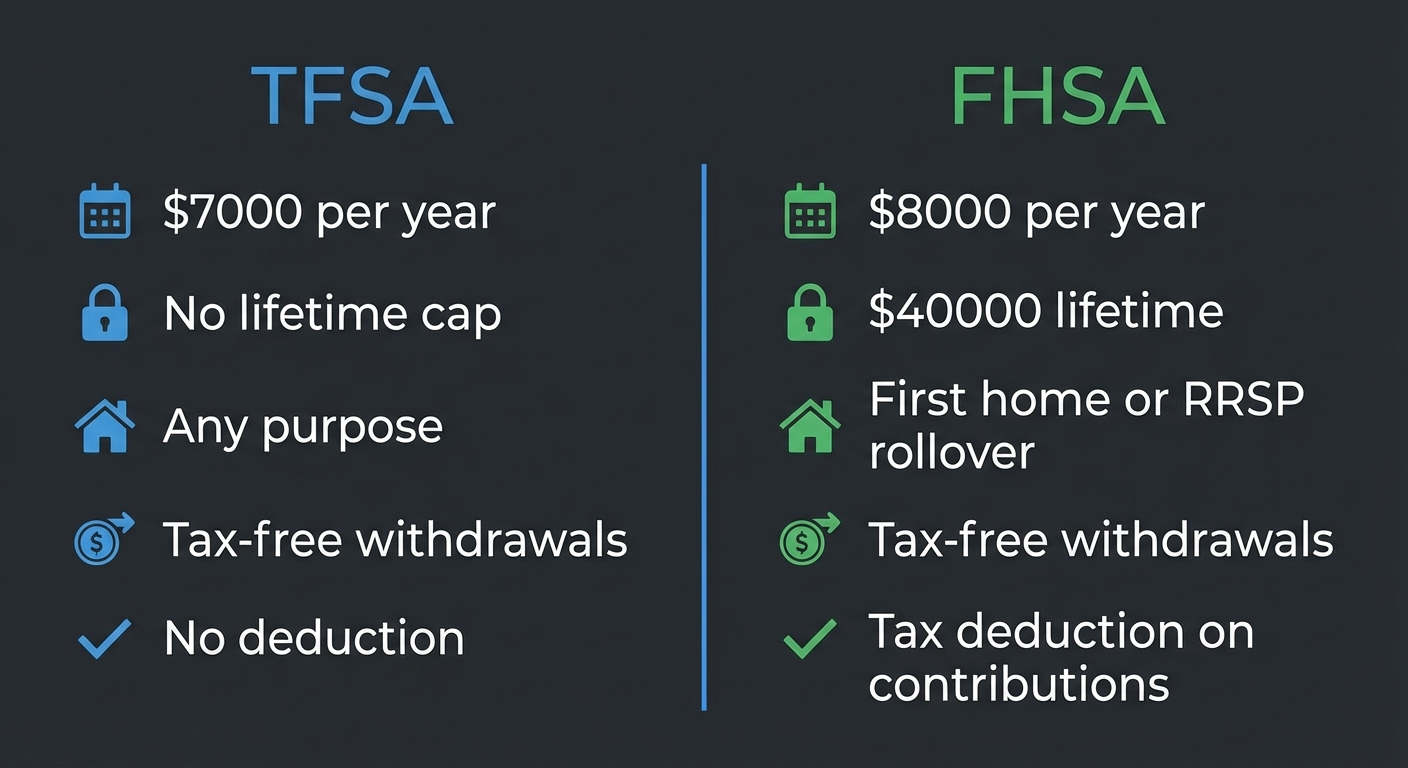

TFSA, RRSP, or FHSA? Here's the honest comparison: what each account actually does, who should open what, and the stacking move that can unlock $200k toward a down payment.

Buy XEQT. Done. Article over. Fine, here's the elaboration you asked for: why all-in-one ETFs beat mutual funds by six figures, and why you're overthinking this.

Most 30-year-old Canadians have saved about $22,000. The benchmark says you should have 1x your salary. Here's what the numbers actually mean and what to do if you're behind.

You don't have to choose between your TFSA and FHSA. Here's how to fund both at the same time, why the FHSA should get the first dollar, and the 15-year deadline most people miss.

Over-contributed to your TFSA? The penalty is 1% per month. Here's exactly how to fix it, how to request a CRA waiver, and how to make sure it never happens again.

The 2026 RRSP contribution limit is $33,810. Here's what that actually means for you, how to calculate your personal room, and whether you should max it out this year.

The TFSA and FHSA look similar but they are different tools for different jobs. If you qualify for both, you should have both. The question is not which one. It is which one first.

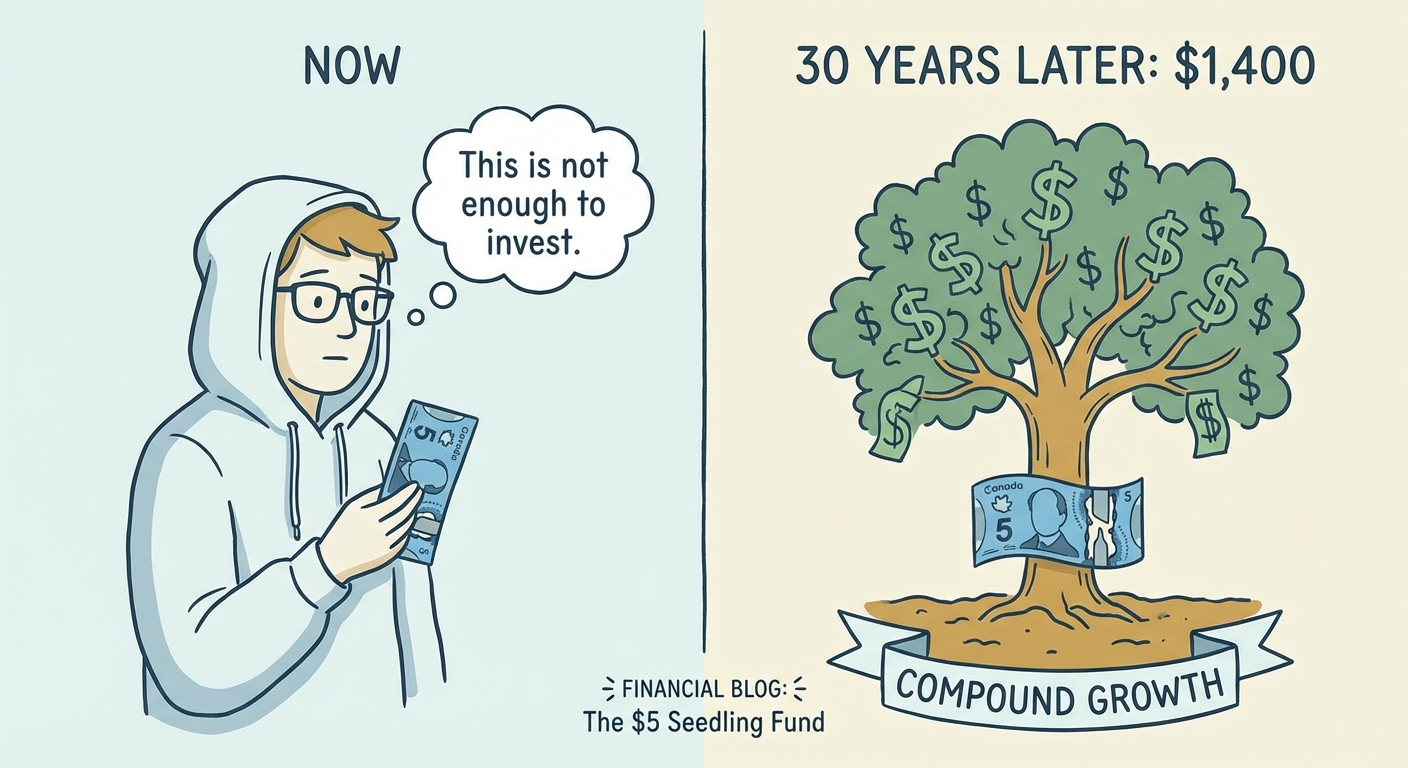

The biggest lie in Canadian personal finance is that investing is for people who have money to spare. Fractional shares, zero commissions, and one ETF have made $25 a paycheck a legitimate wealth-building strategy. Here is the math.

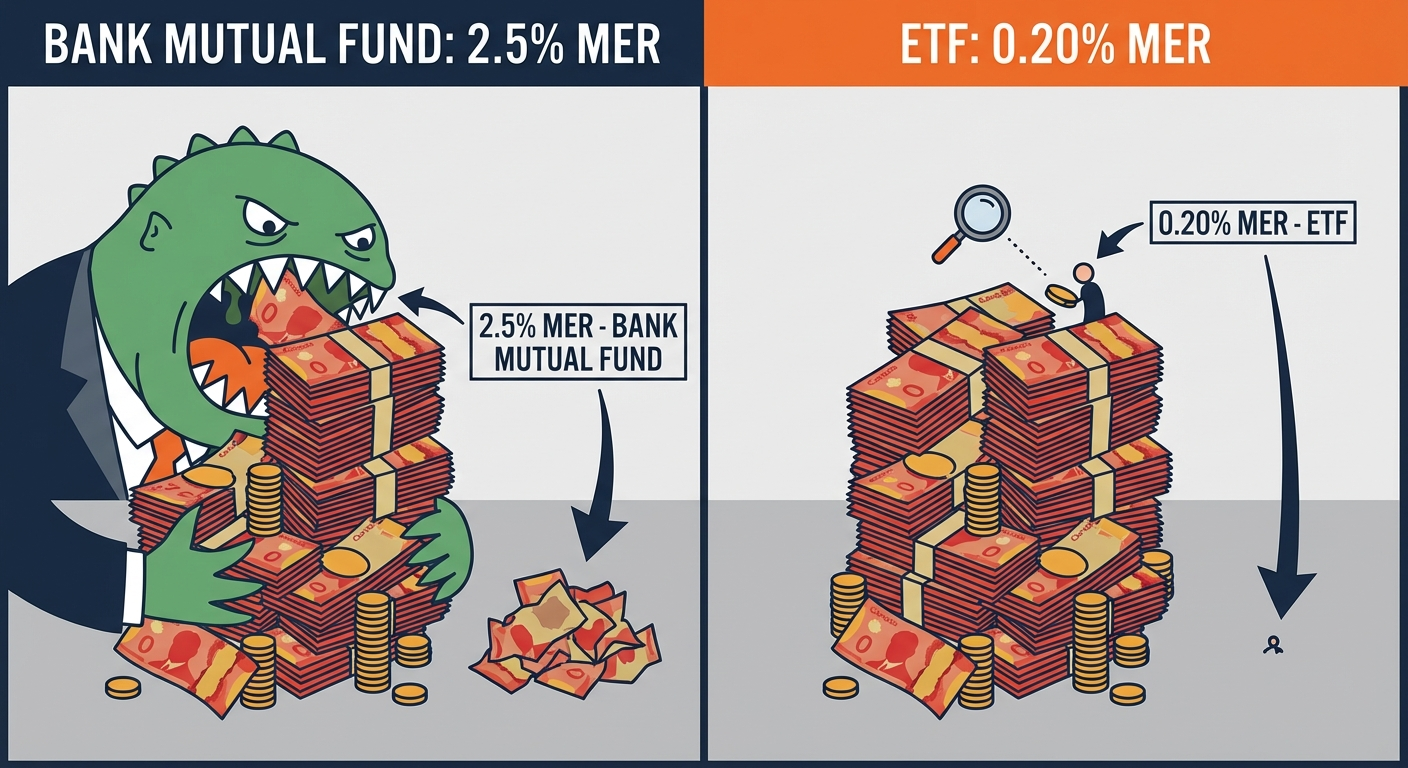

Canada has some of the highest mutual fund fees in the world. It is not an accident. It is a system that pays your advisor to keep you in expensive funds. Here is how it works and what to do about it.

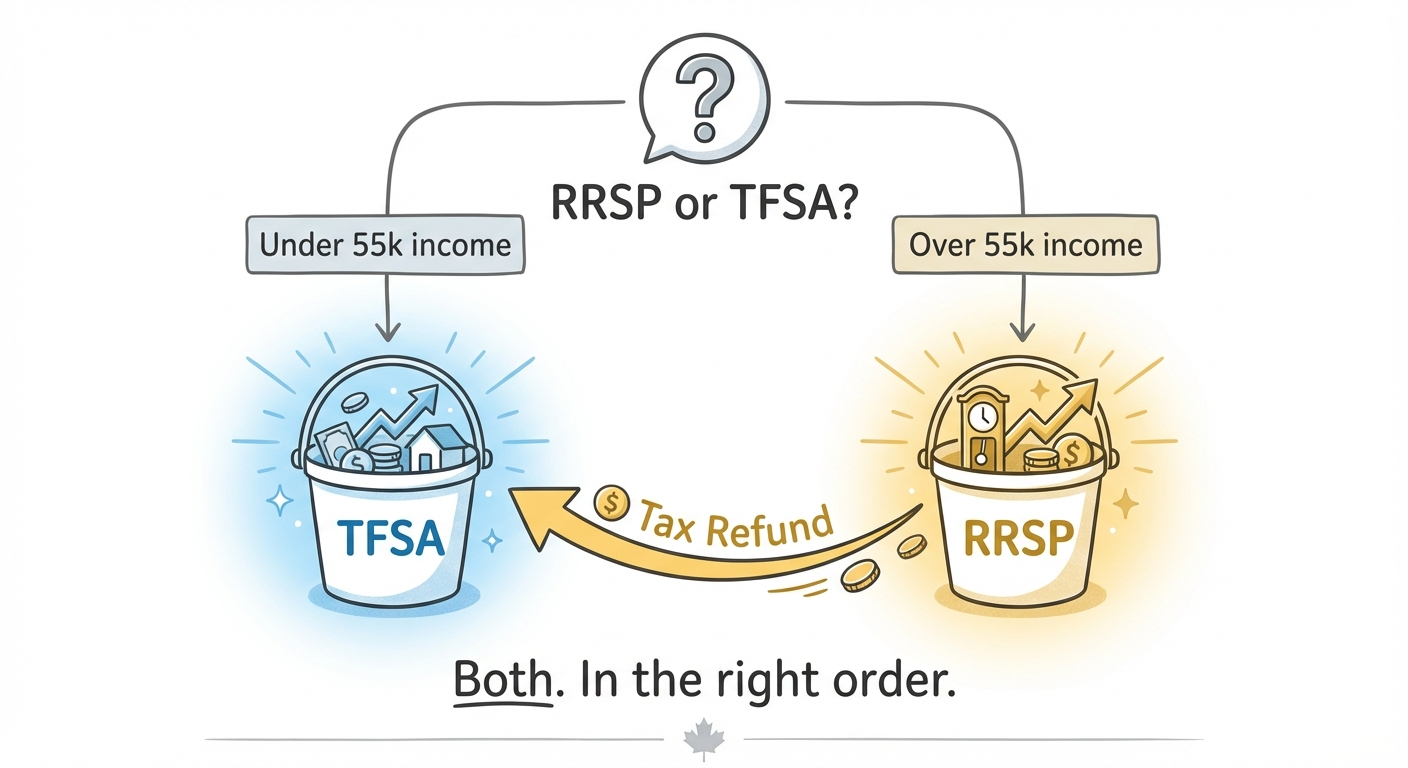

RRSP or TFSA first? Use your income, employer match, goals, and 2026 contribution limits to decide where your next dollar should go.

Most Canadians have a TFSA. Most Canadians are leaving it in a savings account earning almost nothing. Here is the one thing to buy instead, and the math on why it matters.

Most Canadians think the FHSA is only useful if you're saving for a home. That assumption is costing them thousands. Here's how the FHSA wins whether you buy a house or not.

Why TFSA should be changed to Tax Free Investment Account