RRSP or TFSA: Which Do You Fill First?

There are two answers to this question. One is correct. The other is what your bank tells you.

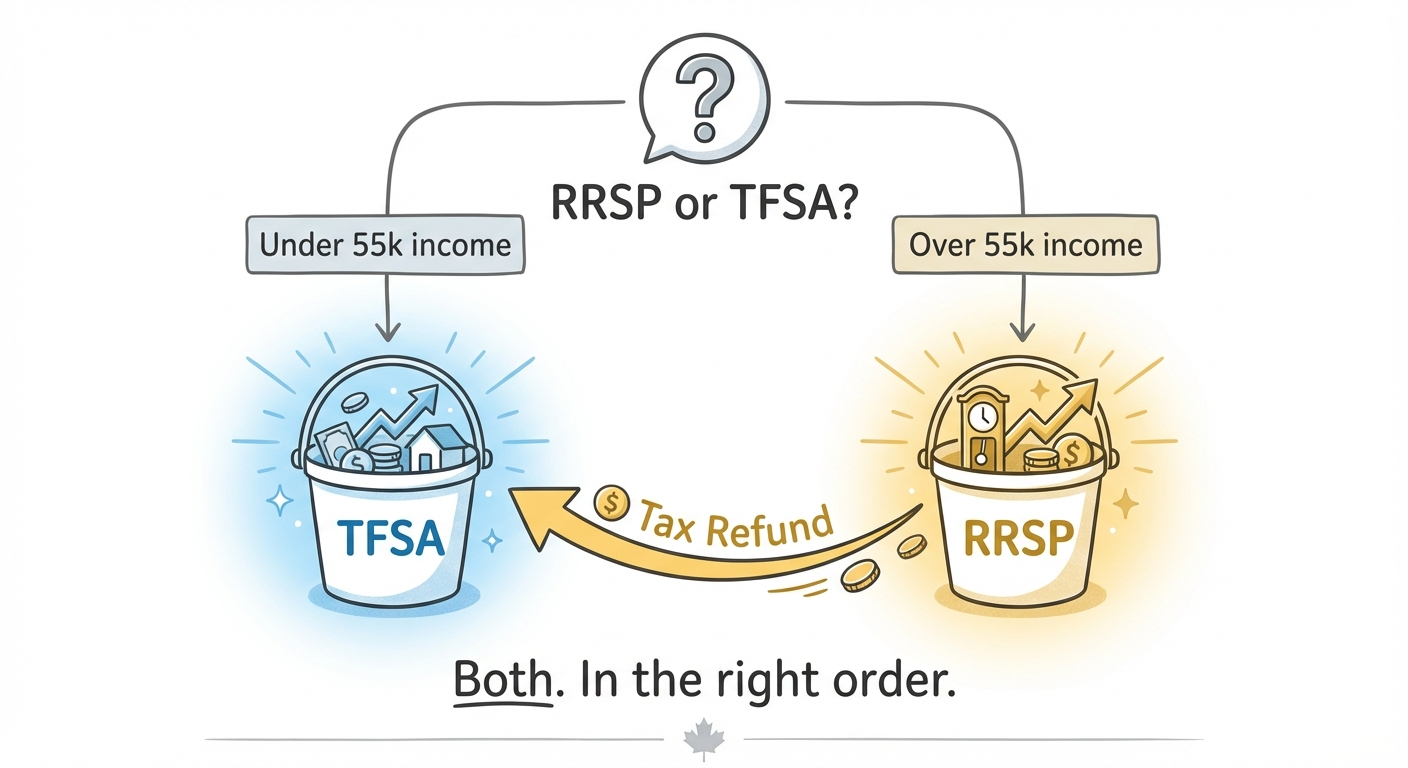

The correct answer depends entirely on your income. Not your age, not your timeline, not your feelings about homeownership. Your income. Once you know which bracket you are in, the decision is not complicated. It is arithmetic.

The Problem: 'It Depends' Is Not an Answer

Every piece of RRSP vs TFSA content online eventually lands on: 'It depends on your situation.' That is technically true. It is also completely useless advice. Of course it depends. Everything in personal finance depends. The question is: depends on what, exactly, and what do I actually do?

The answer is one variable: your marginal tax rate now versus your expected marginal tax rate in retirement. If you are in a higher bracket today than you will be when you retire, the RRSP wins. If you are in a lower bracket today, or expect to be in roughly the same bracket in retirement, the TFSA wins. Everything else is noise.

The Insight: The Income Threshold That Actually Matters

Here is the practical breakdown based on 2026 federal tax brackets:

- Under roughly $55,000 in income: Open and fill your TFSA first. At this income level, your marginal federal tax rate is 14%. Adding provincial tax, you are likely in the 20-30% combined bracket. The RRSP deduction saves you those cents on the dollar, which is decent, but not enough to justify locking the money away until retirement. The TFSA lets you withdraw without penalty at any income level, so if you need the money before 65, it is not a tax event. The RRSP is. That flexibility matters when you are still building.

- Between $55,000 and $100,000: RRSP first, but here is the important nuance: you only contribute enough to bring your taxable income down to the $58,523 bracket threshold, not your full RRSP room. For example, if you earn $65,000, you only need to contribute $6,477 to drop into the lower bracket and maximize your refund per dollar. Contributing beyond that still builds retirement savings, but the tax saving per dollar drops. Figure out your exact number with our RRSP contribution calculator, then put anything left over into your TFSA.

- Over $100,000: Max the RRSP aggressively before anything else. At this income, your combined marginal rate is north of 43% and can hit 54% in some provinces. The RRSP deduction is extraordinarily powerful at this level. Every $10,000 contributed could return $4,300 to $5,400 as a tax refund. That is free money you are declining if you contribute to the TFSA first. Use our RRSP calculator to find your exact optimal contribution.

The Power Move: RRSP Plus Refund Into TFSA

If you earn over $55,000, here is the exact sequence that makes both accounts work together:

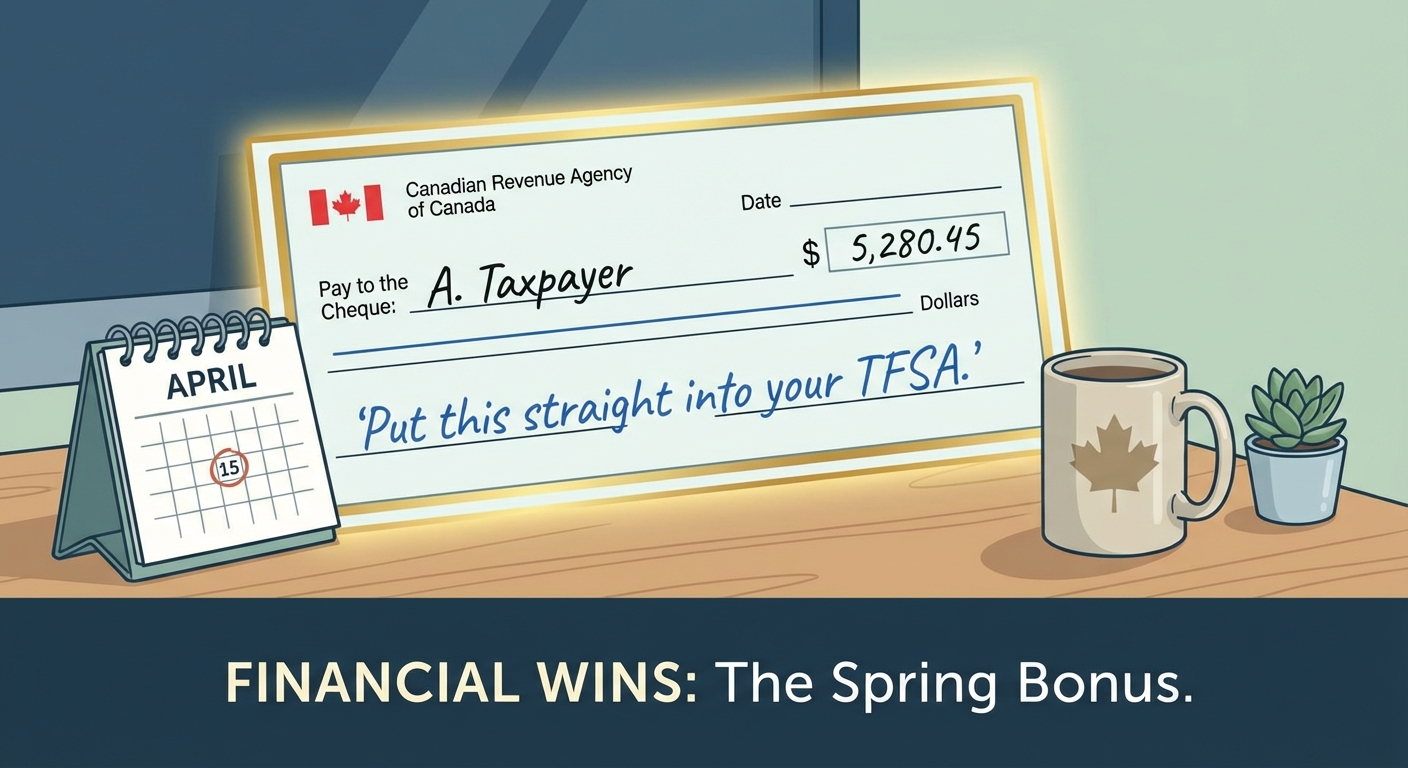

- Contribute to your RRSP before the deadline (60 days into the new year, so around March 1).

- File your taxes. Your RRSP contribution reduces your taxable income. The CRA sends you a refund.

- Take that refund and put it into your TFSA. Do not use it for anything else. Do not buy a TV. Put it in the TFSA immediately, invested in XEQT or VGRO.

- Repeat every year. You are now compounding in two tax-sheltered accounts simultaneously, using the government's own refund mechanism to fund the second one.

This is not a loophole. This is exactly how these accounts are designed to work together. The government built the refund mechanism. Use it.

What To Actually Do

- Check your income for this year and determine which bracket you fall into.

- Under $55k: Open a self-directed TFSA at Wealthsimple or Questrade. Contribute up to $7,000 for 2026, plus any unused room from previous years. Not sure what to buy inside it? We covered exactly that in What Should I Actually Buy Inside My TFSA? Short answer: XEQT or VGRO.

- Over $55k: Contribute to your RRSP before March 1, but only contribute the amount needed to bring your taxable income down to $58,523. Anything above that threshold still helps, but the per-dollar tax saving drops. Use our RRSP calculator to find your ideal number. File your taxes, wait for the refund, put the refund straight into your TFSA.

- Check your limits first. Log into CRA My Account to see your exact TFSA room and RRSP deduction limit. These numbers are specific to you. Do not guess them.

- Do not overthink the order. A dollar in either account, invested in a broad-market ETF, is worth vastly more over 30 years than a dollar sitting in a bank savings account regardless of which account holds it. The worst move is paralysis.

The RRSP and TFSA were not designed to compete with each other. They were designed to work together. One cuts your taxes today. The other protects your gains forever. Figure out your income, make the call, and stop leaving free money on the table.

2026 RRSP Contribution Limit: What You Need to Know

The 2026 RRSP contribution limit is ,490. This is the maximum you can contribute to your RRSP in 2026, before factoring in your unused carry-forward room from previous years. The limit increases each year based on inflation, so if you have been maxing out your RRSP every year, you have a bit more room this year than last.

Your actual RRSP contribution room for 2026 is 18% of your 2025 earned income, up to the ,490 limit, plus any unused room you have been carrying forward from previous years. Check your most recent NOA (Notice of Assessment) from the CRA to find your exact carry-forward amount.

RRSP vs TFSA Contribution Limits for 2026

The 2026 TFSA contribution limit is ,000, the same as 2024 and 2025. If you have never contributed to a TFSA and have been a Canadian resident since 2009 (when the TFSA launched), your cumulative TFSA room in 2026 is ,000. Compare that to the RRSP where your room depends entirely on your income history.

So which do you fill first in 2026? The answer has not changed: if your income is above ,000, prioritize the RRSP for the tax deduction. If your income is below ,000, or if you are saving for a flexible goal, the TFSA is usually the better first move. Use our RRSP contribution room calculator to find your exact 2026 limit before you contribute.

Free guide

Get the TFSA vs RRSP vs FHSA decision guide.

Join for practical Canadian investing guides, calculators, and plain-English account strategy updates. No spam, unsubscribe any time.