What Should I Actually Buy Inside My TFSA?

Your TFSA is probably losing you money right now. Not because the market is down. Because your bank quietly put it in a savings account earning 1.5% and nobody told you that you could do something dramatically better with it.

Most Canadians have a TFSA. Most Canadians treat it like a high-interest savings account. Those two facts explain a lot about the wealth gap between people who know how registered accounts actually work and everyone else.

The Problem: Your Bank Set You Up to Lose Slowly

When you opened your TFSA at your bank, a very friendly person probably showed you a savings account or a GIC. Maybe a mutual fund if you seemed like you had money. You signed some forms. The account existed. You felt responsible.

Here is what they did not explain: the TFSA is a container, not a product. What you put inside the container is completely up to you. Your bank defaulted you into their products because that is how banks make money, not because those products are right for you.

The average Canadian mutual fund charges a Management Expense Ratio (MER) of around 2% to 2.5% per year. An MER is the annual fee you pay just to hold the fund, whether it goes up or down. You do not see it as a line item. It is silently deducted from your returns every single year. It is the financial equivalent of a subscription you forgot you signed up for, except it costs you more every year as your balance grows.

The Insight: One ETF. One Purchase. Done.

An ETF, or Exchange Traded Fund, is simply a basket of hundreds or thousands of stocks bundled into a single ticker symbol you can buy like a regular stock. A good all-in-one ETF like XEQT holds thousands of companies across Canada, the US, Europe, and emerging markets in a single purchase. You buy one thing. You own a tiny piece of the entire global economy.

XEQT, made by iShares (BlackRock), charges an MER of 0.20% per year. VEQT from Vanguard charges 0.24%. These are not rounding errors. This is a real, structural difference in how much of your money you actually keep.

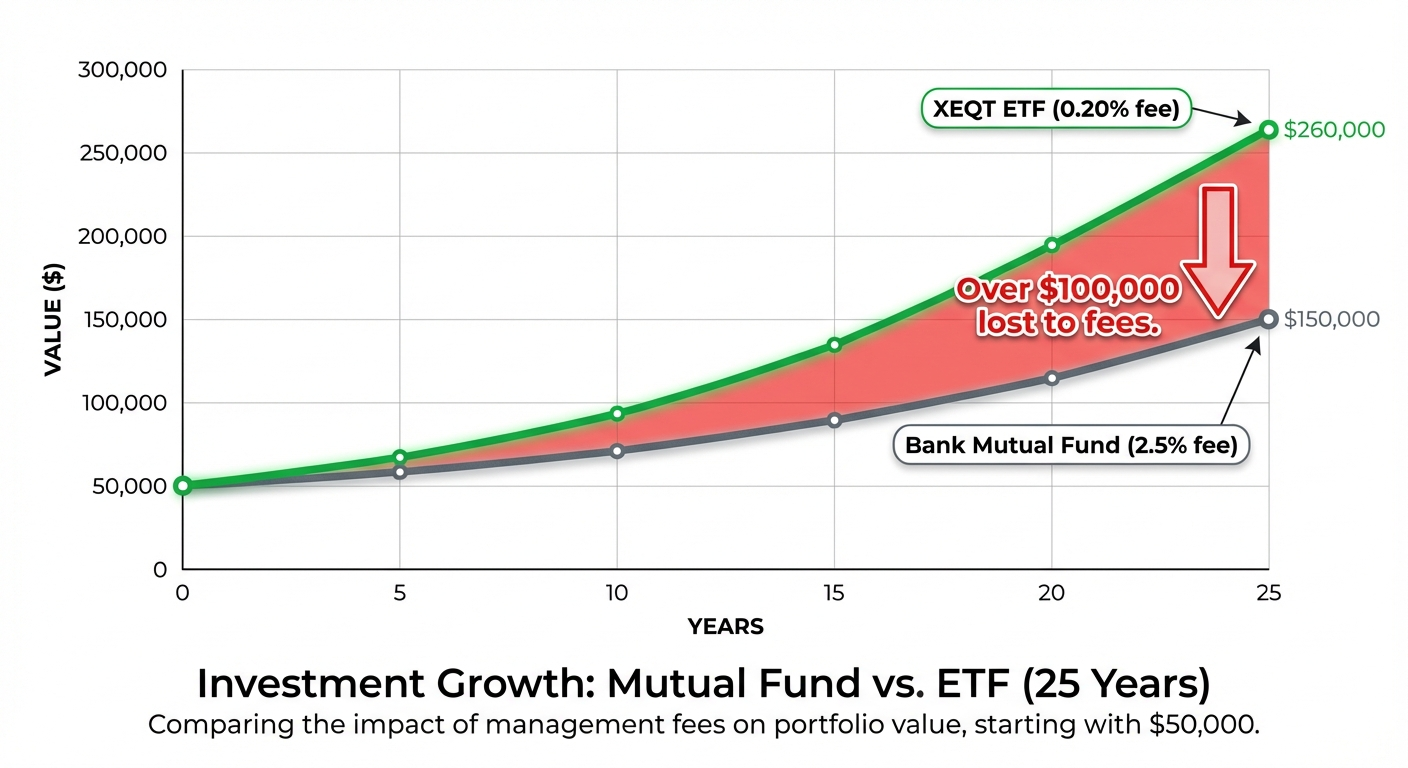

Here is the math with a real example. Take $50,000 invested for 25 years, assuming a 7% gross annual return before fees.

- Bank mutual fund at 2.5% MER: net return of 4.5%, final value roughly $150,000.

- XEQT at 0.20% MER: net return of 6.8%, final value roughly $259,000.

- The difference: over $108,000. Paid in fees. To a bank that also charges you $16.95 a month to hold your chequing account.

The bank sends you a calendar in December. You have paid for approximately 1,000 calendars.

Which ETF Should You Actually Buy?

For most people reading this, the answer is one of two options:

- XEQT (iShares Core Equity ETF Portfolio, 0.20% MER): 100% equities. Holds thousands of stocks globally. Best for long-term investors with 10 or more years before they need the money. If you are under 45 and are not touching this for decades, this is your default.

- VGRO (Vanguard Growth ETF Portfolio, ~0.24% MER): 80% equities, 20% bonds. Slightly smoother ride during market downturns. Good if you are 5 to 10 years from needing the money and want a bit less volatility without going fully conservative.

The difference between these two is not as important as the decision to buy one of them instead of a bank mutual fund. Stop optimizing the choice. Make the choice.

What To Actually Do

- Open Wealthsimple or Questrade and open a self-directed TFSA. This takes about five minutes on your phone. The account is free.

- Transfer or contribute to your TFSA. Check your available contribution room first at CRA My Account. Do not guess this number.

- Search for XEQT or VGRO. Buy as many shares as your contribution allows. If you are on Wealthsimple, trades are free. If you are on Questrade, ETF purchases are free.

- Set up a recurring contribution. Every payday, automatically move money in and auto-buy. Remove the decision from the equation entirely.

- Stop checking it. Seriously. You are investing for decades. Looking at it daily is not a strategy, it is anxiety. The market will go down. Keep buying. That is the strategy.

Your TFSA was designed to be one of the most powerful wealth-building tools in Canada. Your bank turned it into a savings account. You can fix that in about five minutes. The bank will still send you a calendar. You just won't need their financial advice anymore.

Free guide

Get the TFSA vs RRSP vs FHSA decision guide.

Join for practical Canadian investing guides, calculators, and plain-English account strategy updates. No spam, unsubscribe any time.