Why Is Your Mutual Fund Quietly Stealing From You?

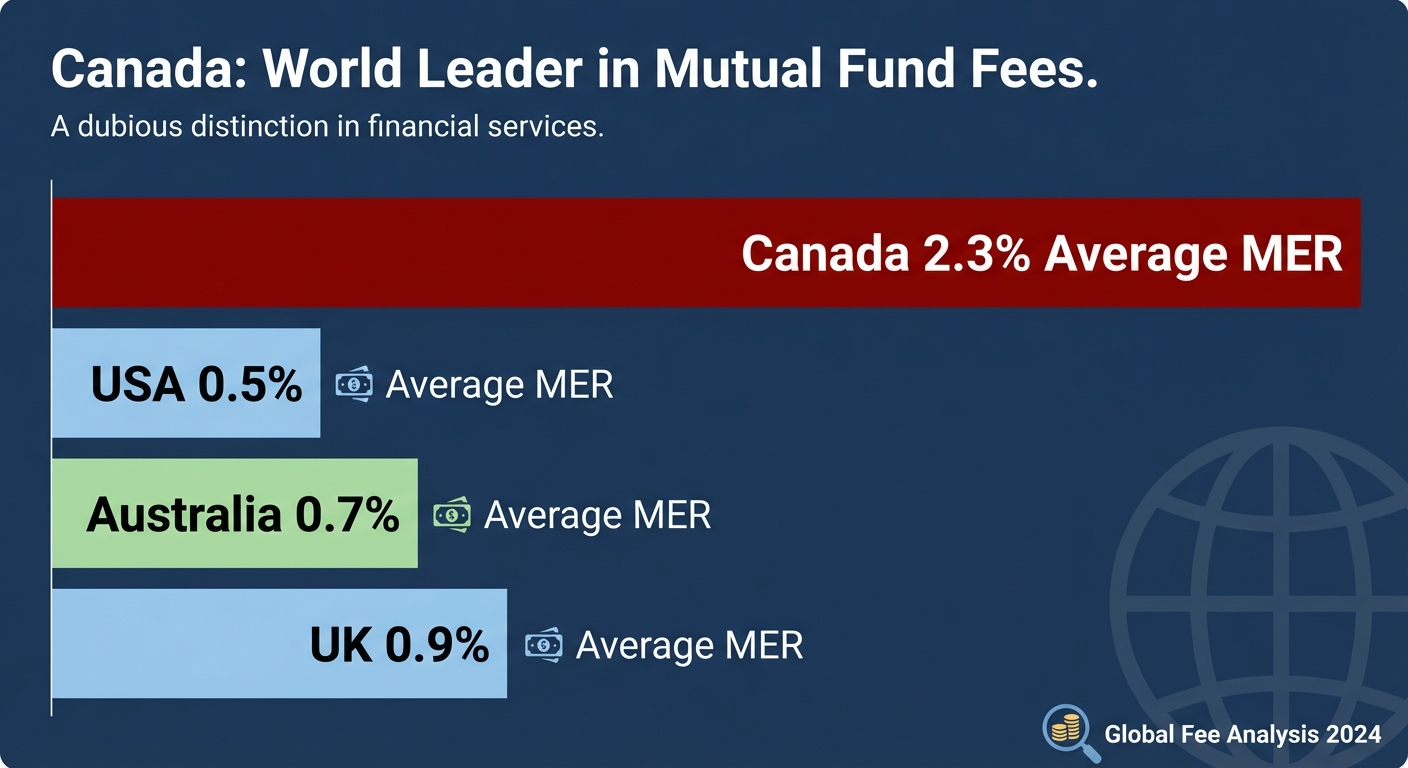

Canada has among the highest mutual fund fees in the world. The average Canadian mutual fund charges a Management Expense Ratio of around 2% to 2.5% per year. The global average is closer to 0.5%. This is not a coincidence. It is the predictable result of a system that was designed to pay your financial advisor, not to maximize your returns.

Your fund is not performing badly because of bad luck. It is performing badly because a significant portion of your investment is being siphoned off every single year to pay the people who recommended it to you. This has been going on for decades. Most Canadians have no idea it is happening.

The Problem: The Fee You Cannot See

A Management Expense Ratio (MER) is the annual percentage fee charged to operate a mutual fund. It covers management, administration, marketing, and, crucially, something called a trailer fee. It is deducted directly from the fund's assets before your returns are calculated. You never see it as a line item on your statement. It is invisible by design.

Here is the math on invisible. If your mutual fund has a 2.3% MER and the market returns 7% in a given year, your fund reports a return of roughly 4.7%. You see 4.7% on your statement. You think: not bad. You do not see the 2.3% that quietly left your account. You did not authorize it as a separate transaction. You signed it away when you agreed to hold the fund.

The Insight: Who Is Actually Getting Paid

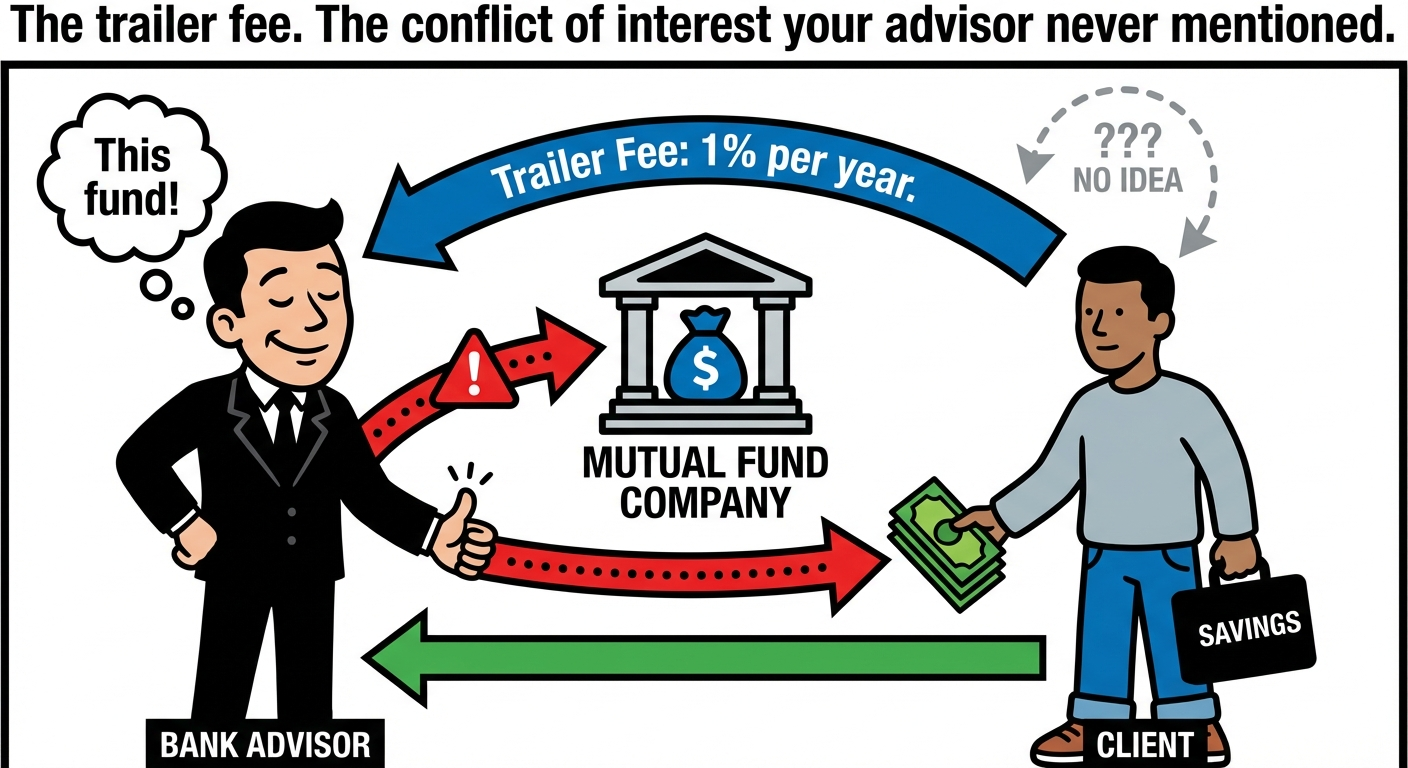

Inside that 2% to 2.5% MER is a fee most Canadians have never heard of: the trailer fee. It is typically around 1% of your balance per year, paid by the mutual fund company directly to the financial advisor who recommended the fund. Every year. As long as you hold it.

Your advisor does not charge you an invoice. They are paid by the fund company for keeping your money in their product. This creates a straightforward conflict of interest: the advisor who recommends the most expensive fund gets paid the most. The fund that is best for you and the fund that is best for their income are not necessarily the same fund.

Canada partially addressed this by banning embedded commissions for some distribution channels starting in 2022. But embedded trailer fees remain pervasive in bank-sold mutual funds, which is where most Canadians still hold their investments. The reform was real. The problem is not solved.

What This Costs You Over a Career

Take $100,000 invested for 30 years at a 7% gross annual return:

- At 2.3% MER (bank mutual fund): net 4.7% return, final value roughly $394,000.

- At 0.20% MER (XEQT): net 6.8% return, final value roughly $730,000.

- The difference: $336,000. Paid in fees over 30 years. That is not a rounding error. That is a retirement.

The advisor who recommended the expensive fund will have moved on long before you do the math in retirement. You will not.

What To Actually Do

- Find out what you are holding. Log into your investment account and look up the MER of every fund you own. If it is above 0.5%, you are paying too much.

- Switch to a self-directed account. Open a TFSA or RRSP at Wealthsimple or Questrade. Both are free to open. ETF purchases at Questrade are free. Trades at Wealthsimple are free.

- Buy one all-in-one ETF. XEQT (100% equity, 0.20% MER) or VGRO (80% equity, 0.24% MER). Buy it. Set up a recurring purchase. Stop paying someone else to do this for you.

- If you want advice, pay for it directly. A fee-only financial planner charges you a flat fee for a financial plan. They are not paid by the funds they recommend. That is the advice model that actually aligns with your interests.

The Canadian mutual fund industry is not built around your retirement. It is built around fund company revenue and advisor compensation. Those incentives have produced some of the highest retail investment fees in the developed world. Knowing this does not require you to be angry. It just requires you to stop funding it.

Free guide

Get the TFSA vs RRSP vs FHSA decision guide.

Join for practical Canadian investing guides, calculators, and plain-English account strategy updates. No spam, unsubscribe any time.