The RRSP Home Buyers' Plan: How to Raid Your Retirement Savings (Legally) to Buy a Home

You have been told your whole life not to touch your RRSP before retirement. The Home Buyers' Plan says: actually, go ahead.

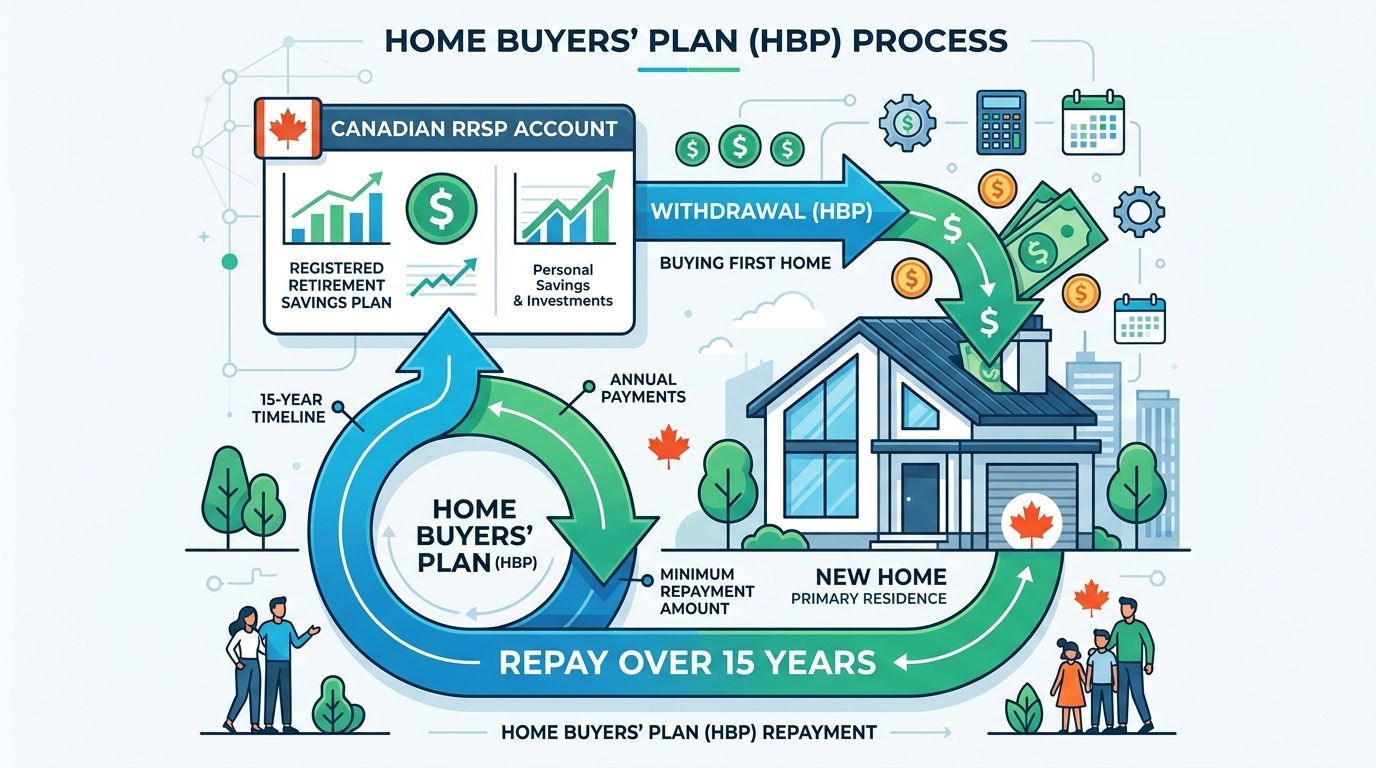

The RRSP Home Buyers' Plan (HBP) is one of the few government programs that does exactly what it sounds like. It lets you pull money out of your RRSP tax-free to buy your first home, then pay it back over 15 years. No immediate tax hit. No penalty. Just cash from your retirement savings going toward a down payment.

If you are sitting on a pile of RRSP money and trying to scrape together a down payment in a Canadian housing market that has not exactly been forgiving, this is worth understanding properly.

What Is the Home Buyers' Plan?

The HBP is a CRA program that allows first-time home buyers to withdraw up to $60,000 from their RRSP to put toward a qualifying home purchase. If you are buying with a partner who also qualifies, you can each withdraw $60,000, for a combined $120,000 toward your down payment.

The withdrawal is not taxed when you take it out. That is the whole point. You already got the tax deduction when you contributed to the RRSP, and as long as you pay the money back within the 15-year window, you do not get taxed on the withdrawal either.

It is essentially an interest-free loan from your future self.

Who Qualifies?

You need to meet a few conditions before you can use the HBP:

You need to be a first-time home buyer. In CRA's definition, that means you have not owned a home that you lived in as your principal residence at any point during the current year or the previous four calendar years. If you owned a home a decade ago but have been renting since, you might qualify again.

You need a written agreement. You must have a written agreement to buy or build a qualifying home before October 1 of the year after your withdrawal.

The home must be your principal residence. You need to intend to live in the home as your main residence within one year of buying or building it.

You must be a Canadian resident. At the time of withdrawal and when you buy the home.

The 90-Day Rule You Cannot Ignore

Here is the one that trips people up most often.

Any money you contribute to your RRSP must sit there for at least 90 days before you can withdraw it under the HBP. If you rush to top up your RRSP right before a home purchase hoping to immediately use that money, it is not going to work. Worse, those rushed contributions may not even be tax-deductible.

So if you are planning to use the HBP, make sure your RRSP contributions are in there well in advance. The strategy works best when you have been building your RRSP for a few years already.

How the Repayment Works

You do not start repaying the HBP immediately. Your repayment period begins the second year after the year you made the withdrawal.

Each year, you are required to repay at least 1/15 of the total amount you withdrew. So if you pulled out $60,000, your minimum annual repayment is $4,000 per year. You can pay back more in any given year if you want to clear it faster.

To designate an RRSP contribution as an HBP repayment, you fill out Schedule 7 when you file your taxes. If you do not make the minimum repayment in a given year, that portion gets added to your income for that year and you pay tax on it. So the repayment is not optional, it is just flexible.

You have 15 years total to pay it all back.

Stacking the HBP with the FHSA

This is where things get genuinely interesting for 2026.

You can use the FHSA and the HBP on the same home purchase. They are not mutually exclusive. If you have been contributing to your FHSA and also have RRSP savings, you can pull from both for the same down payment.

With an FHSA you can withdraw up to $40,000 tax-free and you never have to pay it back. With the HBP you can pull up to $60,000 tax-free and repay over 15 years. A couple using both programs together could access up to $200,000 combined toward a first home.

The FHSA withdrawal is cleaner since there is no repayment required. But if you have already built up significant RRSP savings and opened an FHSA, using both gives you maximum firepower.

Common Mistakes to Avoid

Withdrawing too soon after a home sale. If you sold a home recently and used the HBP to buy again, you could be offside. The CRA requires that your previous HBP balance be fully repaid before January 1 of the year you want to make a new withdrawal.

Not tracking your repayments. Every year you need to file Schedule 7 with your tax return to designate HBP repayments. If you just contribute to your RRSP without designating, the CRA will not automatically apply it to your HBP balance.

Ignoring your spouse's eligibility. Your partner may qualify for the HBP even if you do not, or vice versa. Their first-time buyer status is evaluated separately. Do not assume you are both disqualified just because one of you owned a home years ago.

Rushing contributions before a withdrawal. As mentioned, the 90-day rule exists and it bites people every year. Plan ahead.

Should You Actually Use It?

The HBP is not free money. You are essentially borrowing from your future retirement savings and agreeing to pay it back. The risk is that your RRSP misses out on 15 years of compounding while that money is out of the account.

That said, for most first-time buyers in Canada, the math still works. Getting into the housing market sooner, building equity, and benefiting from potential home appreciation can outweigh the opportunity cost in your RRSP. Every situation is different, so it is worth running the numbers with your specific home price, RRSP balance, and expected investment returns.

If you have the RRSP savings and you qualify, the HBP is a legitimate tool. Just use it with eyes open.

The Bottom Line

The RRSP Home Buyers' Plan lets you borrow up to $60,000 from yourself to buy your first home, with no tax hit as long as you pay it back over 15 years. In 2026, you can stack it with the FHSA for even more purchasing power.

The key rules to remember: you need to be a first-time buyer, the money must be in your RRSP for at least 90 days, and you need a written agreement to buy before October of the following year. Get those right and it is one of the more useful levers in Canadian personal finance.

Free guide

Get the TFSA vs RRSP vs FHSA decision guide.

Join for practical Canadian investing guides, calculators, and plain-English account strategy updates. No spam, unsubscribe any time.