Where Should You Keep Your Emergency Fund in Canada?

If your emergency fund is sitting in your chequing account, that is a bad setup.

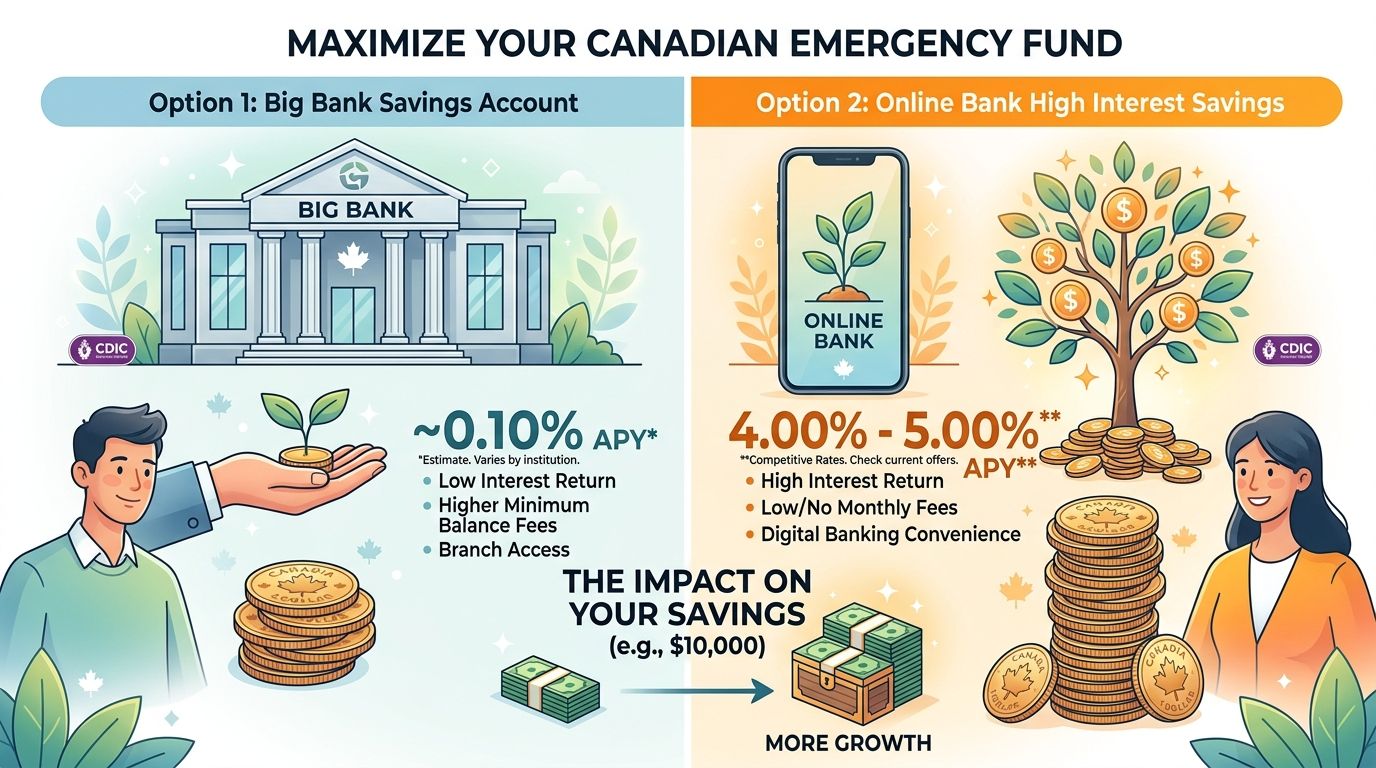

If it is sitting in a regular savings account at one of the big banks earning something insulting like 0.11% or 0.30%, that is an even worse one.

An emergency fund should be safe, easy to access, and actually pay you something for waiting. For most Canadians, the best place for it is a high interest savings account at a separate online bank.

That usually means names like EQ Bank, Tangerine, Simplii, Neo, or another no fee online option with a real savings rate.

This is not the part of your money that needs to be optimized for maximum returns. It is the part that needs to be there when life gets weird. Job loss. Vet bill. Surprise car repair. Last minute flight. Broken furnace. You want it boring, liquid, and untouched.

That is exactly why a high interest savings account works so well.

Quick comparison of emergency fund friendly savings accounts in Canada

| Bank | Rate | Promo or ongoing | Best for | Catch |

| EQ Bank Personal Account | 2.75% with direct deposit, otherwise 1.00% | Ongoing with condition | Set it and forget it savers | Best rate depends on qualifying direct deposit |

| Tangerine Savings | 4.50% | Promo for 5 months | Promo chasers | Ongoing rate drops sharply after the promo |

| Simplii High Interest Savings | 4.50% | Promo for 5 months | Short term parking | Regular rate is much lower after the promo |

| Saven Financial | 2.85% | Ongoing | People who want a stable non promo rate | Less mainstream, fewer people know it |

| Neo Savings | Around 3.00% | Ongoing | Simple decent yield | Product details and rates can change |

| Oaken Financial | Around 2.80% | Ongoing | Conservative savers | Fewer everyday banking features than some competitors |

Rates move around, especially promo rates, so always verify them before you open anything.

What an emergency fund actually needs to do

People sometimes overcomplicate this.

Your emergency fund has three jobs:

- protect you when something expensive happens

- stay available without market risk or lockups

- earn at least enough interest that inflation is not chewing through it quite as fast

That rules out a lot of bad homes for it.

Stocks are too volatile. A GIC can lock your money up. Your chequing account pays nothing. And the default savings accounts at a lot of traditional banks are a bad joke.

You do not need your emergency fund to impress anyone. You need it to quietly work.

Why a high interest savings account is the best fit

A high interest savings account gives you the combination an emergency fund needs:

- your money is not invested in the market

- you can access it when you need it

- you earn more interest than you would in a typical big bank savings account

- most good options have no monthly fee

- eligible deposits are usually covered by CDIC or provincial deposit insurance

That makes it the cleanest answer for almost everyone.

You are not trying to squeeze every last basis point out of your emergency fund. You are trying to protect your downside while still earning something reasonable.

The underrated reason to keep it at a separate bank

This part matters more than people think.

Keeping your emergency fund at a separate bank creates a mental divide.

If the money is sitting right beside your chequing account, it is too easy to treat it like extra cash. A weekend trip starts to feel affordable. A furniture purchase starts to look harmless. A random splurge starts to feel temporary.

But when your emergency fund lives at a separate online bank, there is a small amount of friction. You have to log in. You have to transfer the money back. You usually have to wait a bit.

That delay is not enough to stop you in a real emergency. But it is often enough to stop you from lying to yourself.

That psychological barrier is useful.

It keeps your emergency fund feeling like savings, not spending money with a different label.

Why regular bank savings accounts are so bad

A lot of Canadians assume that if their bank offers a savings account, it must be a reasonable place to keep savings.

It often is not.

Many traditional savings accounts still pay rates so low they are barely worth acknowledging. Some are around 0.30%, 0.55%, or not much better unless you are on a short term promotion. That is not a serious return. That is your bank renting your money for almost free.

Meanwhile, online banks and digital accounts are often paying several times more.

Even if the dollar difference does not make you rich, it matters. If you are keeping 15000 to 25000 dollars in cash for peace of mind, there is no reason to volunteer for an awful rate.

Current high interest savings rates in Canada, April 2026

Rates change constantly, especially promotional ones, but here is the rough landscape as of mid April 2026:

- EQ Bank Personal Account: 2.75% with qualifying direct deposit, otherwise 1.00%

- EQ Bank Notice Savings: 2.35% with 10 day notice or 2.75% with 30 day notice

- Tangerine Savings Account: 4.50% promo for 5 months, with a much lower ongoing rate shown in the savings calculator at 0.70%

- Simplii Financial High Interest Savings Account: 4.50% promo for 5 months, then regular rates depend on balance and are much lower

- Neo Savings Account: around 3.00%

- Oaken Financial Savings Account: around 2.80%

- Saven Financial: around 2.85%, one of the stronger non promotional rates currently tracked

Comparison sites like Ratehub show HISA rates generally ranging from about 1.50% to 4.75%, but the top end is usually a temporary promotion, not a forever rate.

That distinction matters.

Best emergency fund options right now

Best simple option: EQ Bank or Saven.

If you want a straightforward place to park your emergency fund and leave it alone, stable everyday rates matter more than flashy promos.

EQ Bank is easy to set up, fully online, and widely used. The catch is that its best everyday rate depends on setting up direct deposit. Without that, the standard personal account rate drops a lot.

Saven is less famous but currently offers one of the better non promotional rates. For an emergency fund, that kind of consistency is valuable.

Best if you like promo chasing: Tangerine or Simplii.

Tangerine and Simplii both have strong promotional offers right now at 4.50%. That is great if you are willing to watch the calendar and move your money when the offer expires.

But promo rates are not your real long term rate. If you leave the money parked there after the offer ends, your return may drop hard.

That is why I would not blindly recommend a promo rate as the default emergency fund strategy unless you are the type of person who will actually stay on top of it.

Whatever bank you choose, keep your emergency fund somewhere separate from the account you use every day. That structure helps protect the money from you. Not from a crisis. From casual spending.

What I would not do is leave emergency savings sitting in a big bank account paying next to nothing just because it feels familiar.

Should your emergency fund ever be in a GIC?

Usually, no.

The whole point of an emergency fund is access. A non redeemable GIC defeats that.

There are edge cases where someone keeps part of a very large emergency fund in a redeemable GIC or laddered setup, but for most people, the simple answer is this: If you might need the money unexpectedly, do not lock it up.

A high interest savings account is usually the better tool.

For most Canadians, the best home for an emergency fund is a high interest savings account at a separate online bank.

It keeps the money safe. It keeps it accessible. It earns something real. And just as importantly, it makes it a little harder to raid when the thing calling your name is not actually an emergency.

Your bank should not get to pay you crumbs for the privilege of holding money you are being responsible enough to save.

Keep reading

Useful next steps

XEQT vs VFV: Which ETF Should Canadians Buy in 2026?

XEQT vs VFV for Canadian investors in 2026. Which ETF belongs in your TFSA or RRSP, how they differ, and the simple answer for long term investors.

Read nextTFSA Maxed Out? Here Is What To Do Next

Once your TFSA is maxed, your next move depends first on your tax bracket, then your home plans, FHSA eligibility, RRSP room, pension, and taxable account needs.

Read nextInvestingInvesting Is Not as Scary as It Feels

Investing feels scary at first, but beginners do not need predictions, charts, or perfect timing. They need diversification, consistency, and time.

Read nextNewsletter

Get new posts in your inbox.

Finance and tech insights for Canadians — no spam, unsubscribe any time.