You Don't Need to Make Good Money to Start Investing. You Need $25.

Nobody told you that you could buy a fraction of an ETF with $25. Nobody told you that Wealthsimple charges zero commission. Nobody told you that putting $25 aside every paycheck for 30 years turns into $61,400. The banks, to be clear, had every reason not to tell you.

You do not need a high income to start investing. You need a phone, a free account, and the decision to start. That is it.

The Problem: Investing Feels Like Something Rich People Do

The word 'investing' carries a lot of baggage. It sounds like something that requires a financial advisor, a significant sum of money, and a solid understanding of how markets work. The Big Five banks have spent decades reinforcing this idea, because they make money when you feel too intimidated to manage your own finances.

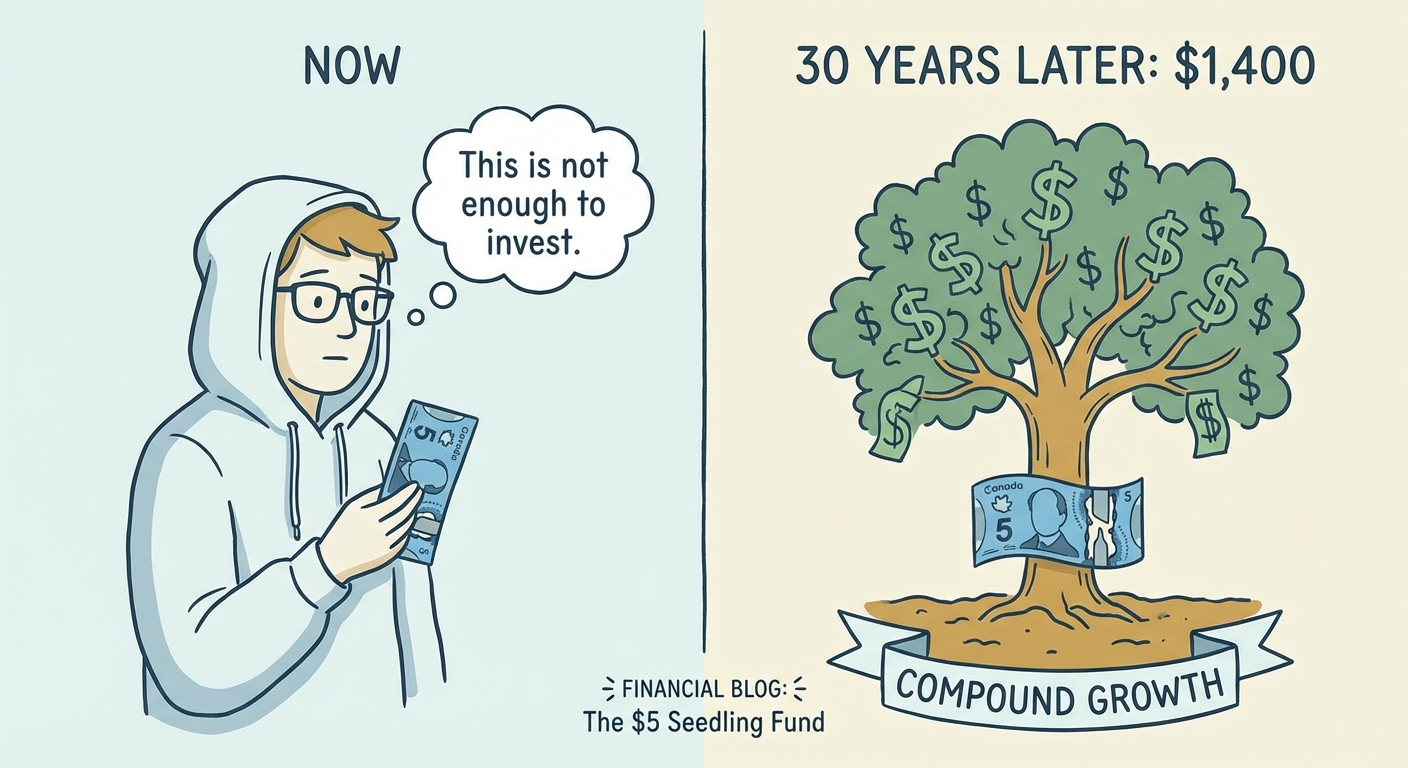

The result is a generation of Canadians who think: 'I'll start investing when I have more money.' That sentence has cost more Canadians more wealth than any stock market crash in history. Because the most powerful force in personal finance is not how much you invest. It is how long you invest.

The Insight: The Math Does Not Care How Much You Start With

Here is what $25 per paycheck actually does over time, invested in a broad-market ETF earning the historical average of around 7% per year:

- After 10 years: $8,981 — from $6,500 contributed.

- After 20 years: $26,647 — from $13,000 contributed.

- After 30 years: $61,400 — from $19,500 contributed.

- After 40 years: $129,763 — from $26,000 contributed.

Double it to $50 per paycheck and the numbers double too: $122,799 after 30 years, $259,526 after 40. From a $39,000 total contribution. The market did the rest.

This is compound interest. It means your gains earn gains. The longer it runs, the more aggressively it works in your favour. Starting 10 years later does not just cost you 10 years of contributions. It costs you the compounding on those contributions for the entire remaining period. Every year you wait is more expensive than the last.

Want to run your own numbers? Use our compound interest calculator to see exactly what your contributions will grow to over time.

What Makes This Actually Possible Now

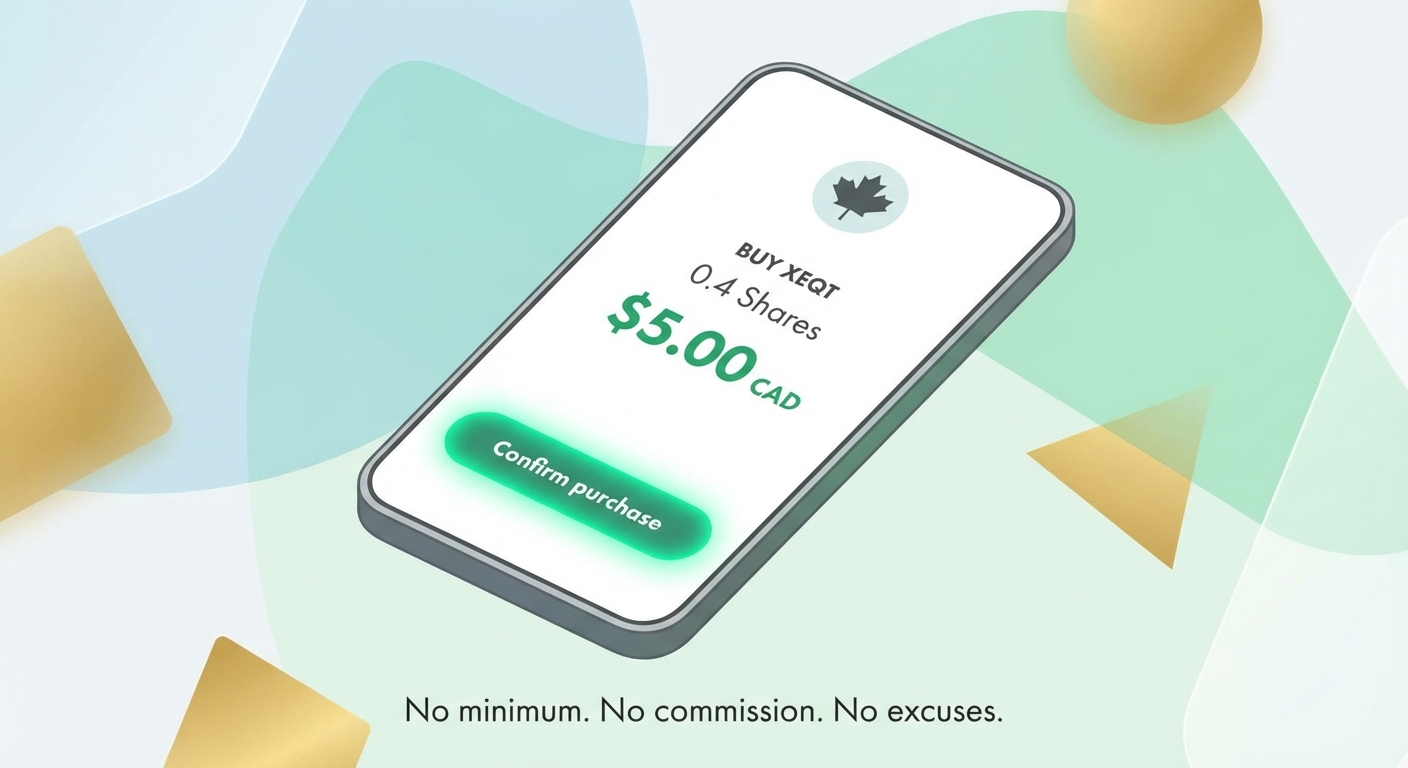

Two things changed investing for everyday Canadians. First, fractional shares. You used to need enough money to buy a full share of whatever you wanted. One share of XEQT today costs around $30-35. But with fractional shares on Wealthsimple, you can invest exactly $25 and own 0.7 of a share. The amount does not need to match the share price. You invest what you have. Second, zero commissions. Wealthsimple charges nothing to buy or sell ETFs. Questrade charges nothing to buy ETFs. The $10-$25 per-trade commissions that used to eat small contributions alive are gone.

This means a $25 investment is now a real investment, not a rounding error swallowed by fees. The minimum viable contribution is whatever you can afford.

What To Actually Buy

For most Canadians starting out, the answer is XEQT — iShares Core Equity ETF Portfolio. It is a single ticker symbol that holds thousands of stocks across Canada, the US, Europe, and emerging markets. You buy one thing. You are instantly diversified across the global economy. The management fee is 0.20% per year. You do not need to rebalance it. You do not need to monitor it. We covered exactly what to buy and why in detail here.

Where To Put It

The account matters as much as what you buy. Put your investments inside a TFSA first if you are under roughly $55,000 in income. Your gains grow completely tax-free and you can withdraw any time without penalty. If you earn more, an RRSP may give you a better tax deduction upfront — and that refund can go straight back into your TFSA. If you are a first-time homebuyer (or even just potentially one someday), an FHSA gives you the tax deduction of an RRSP and the tax-free growth of a TFSA simultaneously.

What To Actually Do

- Download Wealthsimple and open a self-directed TFSA. It takes about five minutes. The account is free.

- Verify your TFSA contribution room at CRA My Account. You likely have significant unused room built up from previous years.

- Set up a recurring deposit of $25 or $50 on every payday. Automate it so it happens without a decision.

- Set it to auto-buy XEQT. Wealthsimple lets you automate recurring purchases. Set it, forget it, let it run.

- Do not check it every day. The market will go down sometimes. That is when you are buying cheaper shares. Keep going.

The best investment account is the one you actually open. The best amount to invest is the one you can actually afford. $25 a paycheck is not too small. It is $61,400 over 30 years, tax-free, doing nothing except existing inside an account your bank never wanted you to open.

Free guide

Get the TFSA vs RRSP vs FHSA decision guide.

Join for practical Canadian investing guides, calculators, and plain-English account strategy updates. No spam, unsubscribe any time.