You Should Open an FHSA Even If You're Never Buying a House. Here's Why.

Yes. Open one today. The rest of this article is just the math.

The First Home Savings Account has a branding problem. The word "home" in the name has convinced an entire generation of Canadians that this account is only useful if you are actively saving for a down payment. That assumption is costing them thousands of dollars. The FHSA is not a home-buying account. It is a tax shelter that happens to offer a bonus if you buy a home. If you never buy one, the account still wins. Quietly. Significantly.

The Problem: Everyone Thinks This Account Has a Catch

Ask most Canadians about the FHSA and they will say some version of: "Oh, that's for people saving for a house, right? I'm not buying anytime soon, so it's not for me."

That is the wrong answer. And it is completely understandable why people get it wrong, because the government named the most flexible tax-sheltered account in Canadian history after the one specific thing you do not have to use it for.

The catch people assume exists is this: if you never buy a home, you lose the money, or get taxed on withdrawal, or face some penalty. None of that is true. There is no catch. There is only upside.

The Insight: The FHSA is a Tax Shelter First, a Home Fund Second

Here is what the FHSA actually does, stripped of the marketing:

- You contribute up to $8,000 per year (lifetime limit: $40,000). That contribution is fully tax-deductible, exactly like an RRSP. If you earn $80,000 and contribute $8,000, the CRA taxes you as if you earned $72,000. That is a real cheque back in your pocket at tax time.

- Every dollar inside grows completely tax-free. Stocks, ETFs, GICs, whatever you hold inside the FHSA, the CRA gets nothing on the gains. No annual tax drag. No capital gains tax. Nothing. This is identical to a TFSA.

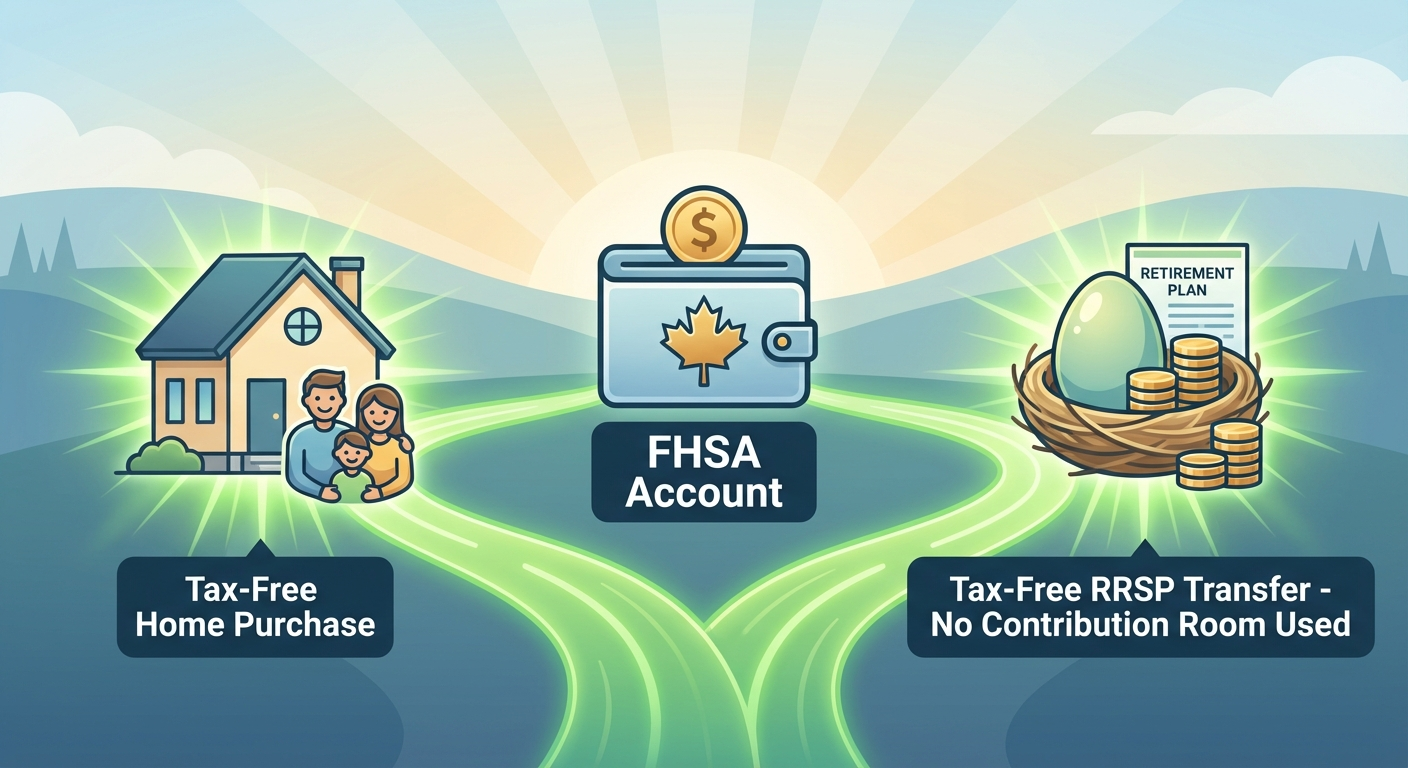

- If you buy a qualifying home, you withdraw everything tax-free. All contributions, all growth, out the door without a dollar of tax. You also do not have to repay it, unlike the RRSP Home Buyers Plan.

Now here is the part nobody talks about.

If you never buy a home, you have up to 15 years from when you opened the account (or until you turn 71, whichever comes first) to transfer everything to your RRSP or RRIF. That transfer is completely tax-free. And it does not consume any of your existing RRSP contribution room. You get to move up to $40,000 of tax-sheltered, already-grown money into your RRSP on top of whatever room you already have. The government is giving you a bonus RRSP top-up for simply having opened an account.

This means the FHSA is not a gamble on homeownership. It is a guaranteed win either way. Buy a house: tax-free withdrawal. Do not buy a house: tax-free transfer to retirement savings, no contribution room touched. The only losing move is not opening one.

What To Actually Do

You do not need to decide whether you are buying a home. You just need to open the account. Here is how:

- Open it now, not when you are ready to buy. The 15-year clock starts the day you open the account, not the day you contribute. Open it today with a $0 balance if you have to. Every month you wait is a month off your clock.

- Use Wealthsimple or Questrade, not your bank. The big banks will put you in expensive mutual funds with management fees that quietly eat your returns. A self-directed FHSA at Wealthsimple takes about five minutes to open on your phone and lets you invest in low-cost ETFs.

- Contribute whatever you can, up to $8,000 this year. Unused room carries forward, up to $8,000 maximum. So if you contribute nothing in year one, you can contribute $16,000 in year two. But the tax deduction only applies in the year you contribute, so earlier is better.

- Invest in broad-market ETFs, not cash. An ETF like XEQT or VGRO gives you instant exposure to thousands of global companies in a single purchase. If your home-buying timeline is more than three years away, there is no reason to hold cash or GICs inside this account. Let it grow.

- Check your TFSA contribution room at CRA My Account first. This is FHSA-specific: you need to confirm you are a first-time homebuyer (meaning you have not owned a qualifying home in the current or previous four calendar years). Most renters qualify automatically.

The FHSA rewards you for saving, grows your money tax-free, hands you a tax refund every year you contribute, and then either buys you a house or boosts your retirement. There is no version of this account where you lose. The government accidentally created a perfect financial product and named it wrong. That is your advantage. Use it.

Free guide

Get the TFSA vs RRSP vs FHSA decision guide.

Join for practical Canadian investing guides, calculators, and plain-English account strategy updates. No spam, unsubscribe any time.