FHSA vs RRSP vs TFSA: The Complete Canadian Account Comparison

Three accounts. Three sets of rules. One very confused Canadian.

If you've ever stared at a comparison chart trying to figure out which one to open first, you're not alone. The names are confusing, the rules overlap, and every bank seems to have a slightly different answer depending on what they're trying to sell you.

Here's the honest version.

The Short Answer

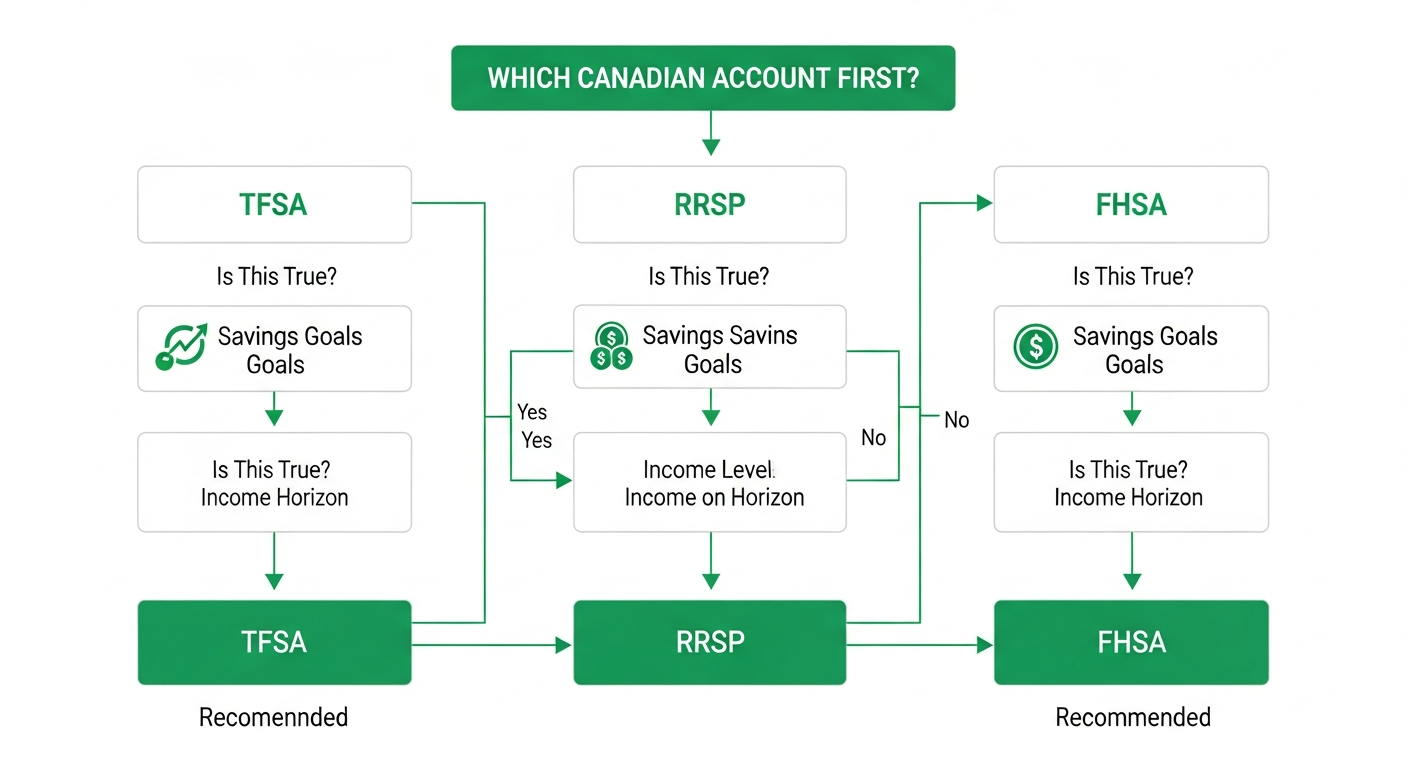

Open a TFSA first if you're young, in a lower income bracket, or unsure about your plans.

Open an FHSA next if you're a first-time buyer saving for a home. Or open one anyway, even if you're unsure, because the worst case scenario is it becomes bonus RRSP room.

Add an RRSP when your income is high enough that the tax deduction is genuinely valuable.

All three can work together. None of them are mutually exclusive. The order just depends on where you are right now.

What Each Account Actually Does

TFSA (Tax-Free Savings Account): $7,000 per year in 2026. If you've been eligible since 2009, total room is $109,000. You contribute after-tax dollars, everything grows tax-free inside, and withdrawals are completely tax-free at any time for any reason. Withdrawals add back to your room the following January 1. Best for flexibility. Works for any goal, any timeline.

RRSP (Registered Retirement Savings Plan): 18% of previous year's earned income, up to $33,810 in 2026. Contributions are tax-deductible, reducing your taxable income today. Everything grows tax-free inside. Withdrawals are taxed as income. Best for high earners who expect to be in a lower tax bracket in retirement. The deduction is worth more the higher your marginal rate.

FHSA (First Home Savings Account): $8,000 per year, lifetime cap of $40,000. Contributions are tax-deductible like an RRSP. Growth is tax-free. Qualifying withdrawals for a first home purchase are completely tax-free. It's the only account that gives you both a deduction on the way in and a tax-free withdrawal on the way out. If you never buy a home, you can transfer the full balance to your RRSP without using any RRSP contribution room — effectively extra RRSP room you wouldn't have had otherwise. Read more in our full FHSA deep-dive.

Head to Head

TFSA vs RRSP vs FHSA at a glance

| Feature | TFSA | RRSP | FHSA |

| 2026 Contribution Room | $7,000/year | 18% of income, max $33,810 | $8,000/year, $40,000 lifetime |

| Tax deduction on contributions | No | Yes | Yes |

| Tax-free withdrawals | Always | No (taxed as income) | Yes, for qualifying home purchase |

| Room carries forward | Indefinitely | Indefinitely | 1 year only (max $8,000) |

| Withdrawals restore room | Yes (Jan 1) | No | No |

| Use for anything | Yes | No | No (home purchase or RRSP transfer) |

| Expires | Never | Convert by age 71 | 15 years after opening or age 71 |

| Best for | Flexibility, any goal | High earners, retirement | First-time buyers (or extra RRSP room) |

Who Should Open What

You're in your 20s, lower income, no specific goal yet: Open a TFSA first. But also consider opening an FHSA even if you're unsure about buying a home. The deduction is useful now, and if you never buy, you can transfer the whole balance to your RRSP later as bonus contribution room. The worst case scenario for the FHSA is still pretty good.

You're saving for your first home: Open an FHSA immediately, even if you can only put in a small amount. The 15-year clock starts at account open, not first contribution. Then complement it with your TFSA.

You're earning $80,000 or more with no home purchase planned: TFSA plus RRSP is the right combination. The RRSP deduction becomes genuinely valuable at higher marginal rates.

You want to buy a home and also save for retirement: All three work together. FHSA first, then TFSA, then RRSP. The FHSA tax refund can go directly into your TFSA. We covered the full strategy in how to maximize both your TFSA and FHSA at the same time.

The Stacking Move Most People Miss

The FHSA and RRSP Home Buyers' Plan can be combined. You can withdraw up to $40,000 from an FHSA for a home purchase (no repayment required). On top of that, the RRSP Home Buyers' Plan lets you withdraw up to $60,000 from your RRSP for a first home purchase, which you repay over 15 years.

A couple who has maximized both accounts could access $200,000 combined toward a down payment. That number changes the math significantly in expensive Canadian cities.

The Simple Framework

TFSA is your flexible foundation. Always open.

FHSA is your home purchase accelerator, or bonus RRSP room if you never buy. Open it now either way.

RRSP is your retirement tax deferral. More valuable the higher your income. Use our RRSP Tax Optimizer to find the contribution that saves you the most.

The accounts are designed to complement each other. You don't have to choose. You just have to know which order makes sense for where you are right now.

Free guide

Get the TFSA vs RRSP vs FHSA decision guide.

Join for practical Canadian investing guides, calculators, and plain-English account strategy updates. No spam, unsubscribe any time.