FHSA Withdrawal Rules in Canada: How Tax-Free Withdrawals Actually Work

If you want to make a tax-free FHSA withdrawal in Canada, you need to meet the CRA qualifying withdrawal rules.

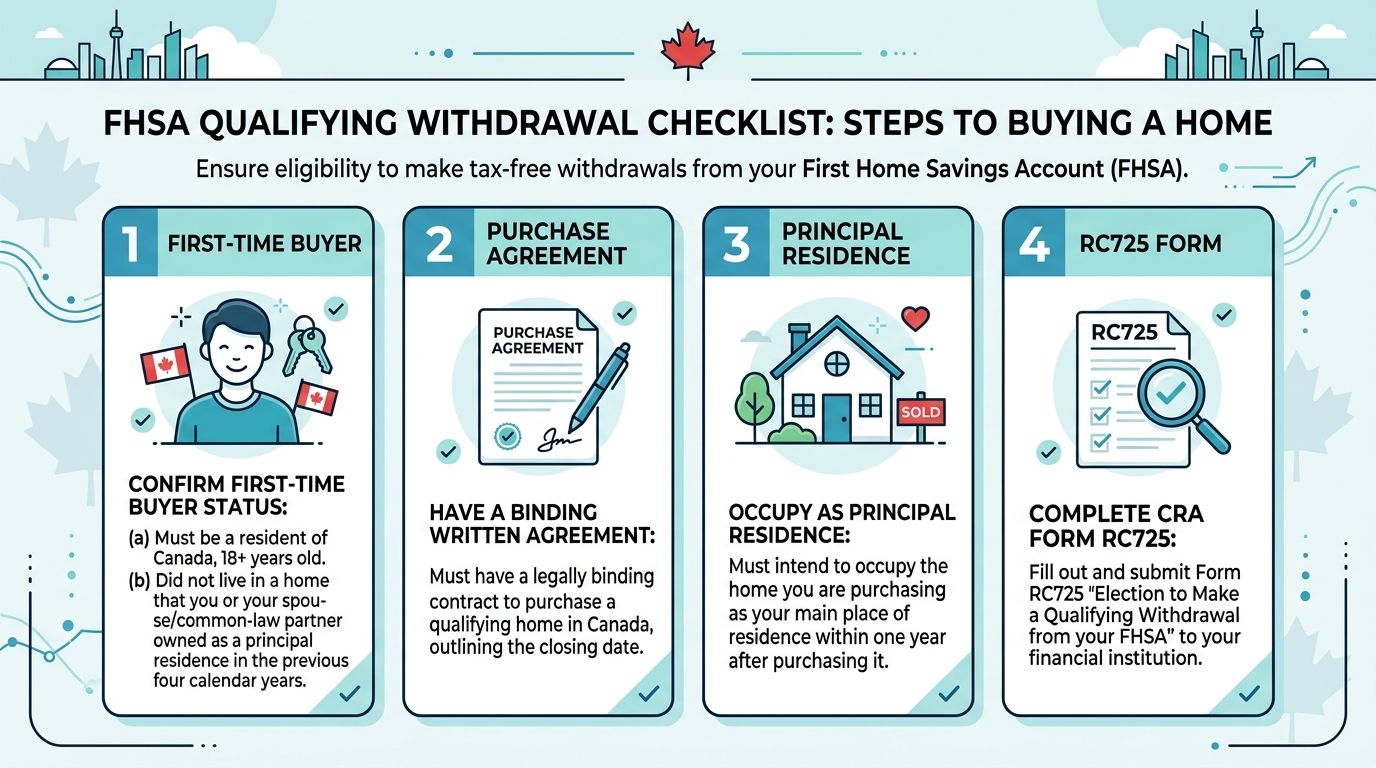

The short version: you must be a first-time home buyer, have a written agreement to buy or build a qualifying home in Canada, intend to move in within one year, and submit the correct form to your financial institution.

If you miss the rules, the withdrawal can become taxable.

FHSA Withdrawal Rules Canada: The Short Answer

- you are a first-time home buyer at the time of withdrawal

- you have a written agreement to buy or build a qualifying home in Canada

- you intend to occupy that home as your principal residence within one year

- you submit Form RC725 to your FHSA issuer

- you make the withdrawal within the CRA allowed time window

What Form Do You Need?

To make a qualifying withdrawal, you must complete CRA Form RC725, Request to Make a Qualifying Withdrawal from your FHSA.

You give this form to your bank or brokerage. You do not send it directly to the CRA.

When Does an FHSA Withdrawal Become Taxable?

- you are not actually eligible as a first-time home buyer

- you do not have a qualifying home purchase lined up

- you take the cash out for another reason

Can You Transfer an FHSA to an RRSP Instead?

Yes. If you do not end up buying a home, you can transfer your FHSA to your RRSP or RRIF on a tax-deferred basis.

That transfer does not use your existing RRSP contribution room.

Bottom Line

If you are buying your first home, have a written agreement, plan to move in, and submit Form RC725 through your institution, your qualifying FHSA withdrawal should be tax-free.

Keep reading

Useful next steps

XEQT vs VFV: Which ETF Should Canadians Buy in 2026?

XEQT vs VFV for Canadian investors in 2026. Which ETF belongs in your TFSA or RRSP, how they differ, and the simple answer for long term investors.

Read nextTFSA Maxed Out? Here Is What To Do Next

Once your TFSA is maxed, your next move depends first on your tax bracket, then your home plans, FHSA eligibility, RRSP room, pension, and taxable account needs.

Read nextInvestingInvesting Is Not as Scary as It Feels

Investing feels scary at first, but beginners do not need predictions, charts, or perfect timing. They need diversification, consistency, and time.

Read nextNewsletter

Get new posts in your inbox.

Finance and tech insights for Canadians — no spam, unsubscribe any time.