TFSA or FHSA: Which One Should You Open First?

Most Canadians treat this as a choice. It isn't.

The TFSA and the FHSA look similar on the surface. Both are registered accounts. Both let your money grow tax free. Both can hold stocks, ETFs, and cash. So people assume they need to pick one, fund it, and move on.

That is not how this works. These are different tools for different jobs, and if you qualify for both, you should have both. The question is not which one. It is which one first.

The Problem: They Look the Same Until You Read the Fine Print

A Tax Free Savings Account (TFSA) lets you invest money, watch it grow, and take it out tax free. You do not get a tax deduction when you put money in. You just never pay tax on whatever the money earns. You can use the money for anything: a vacation, a car, retirement, or nothing. It sits there, growing, no questions asked.

A First Home Savings Account (FHSA) does the same thing. Money goes in, grows tax free, comes out tax free. But only if you use it to buy your first home. If you do not buy, you can roll it into your RRSP without using your RRSP contribution room.

The critical difference is what happens when money goes in. TFSA contributions give you nothing. FHSA contributions reduce your taxable income, the same way RRSP contributions do.

That one detail changes everything.

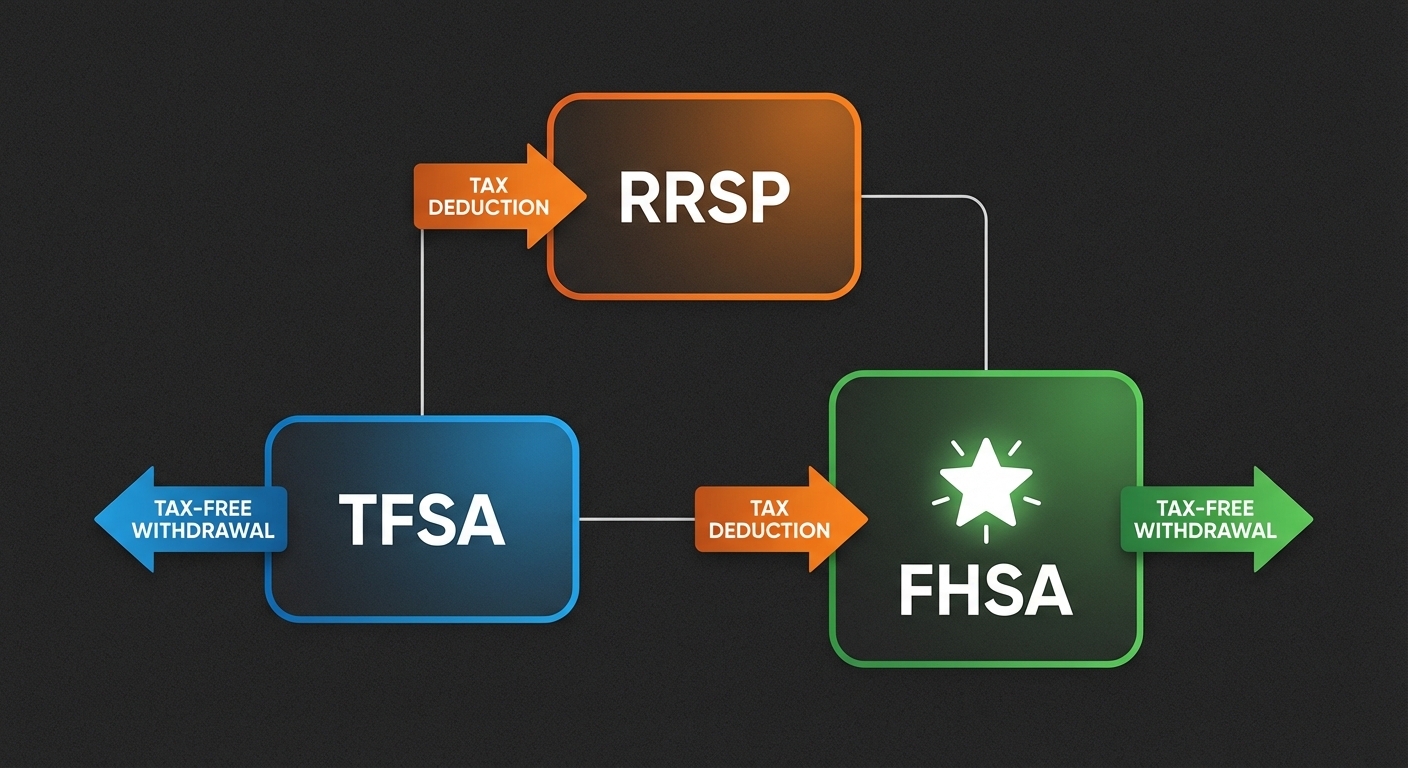

The Insight: The FHSA Is the Best Parts of Both Other Accounts

The RRSP gives you a tax deduction on the way in. The TFSA gives you tax free withdrawals on the way out. The FHSA gives you both: a deduction when you contribute and no tax when you withdraw for a qualifying home purchase.

The government basically combined the two most powerful investing accounts in Canada, added a $40,000 lifetime limit and a first home condition, and called it a day. Quietly one of the best deals in the Canadian tax code.

Here is what the FHSA actually looks like:

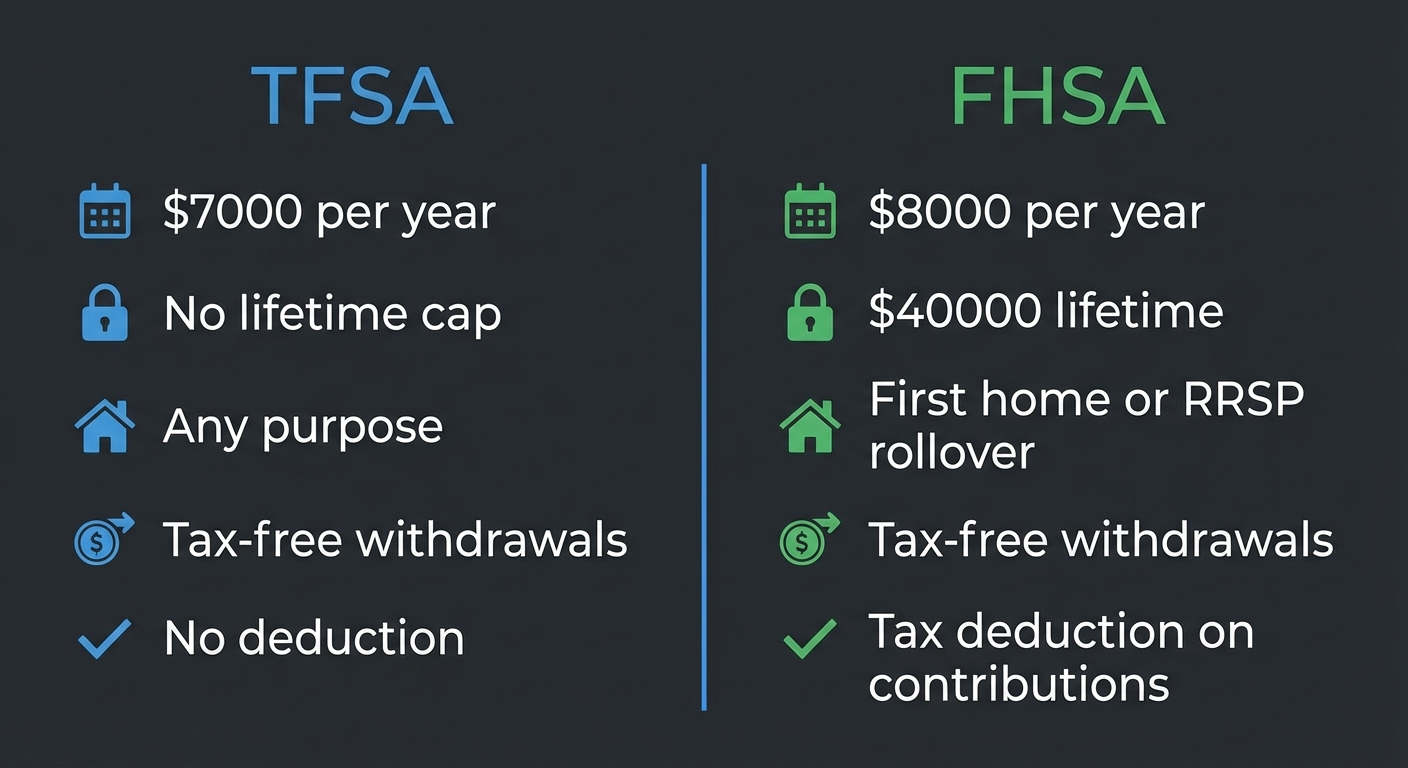

- Annual limit: $8,000 per year

- Lifetime limit: $40,000

- Carryforward: Up to $8,000 of unused room carries forward one year. You cannot accumulate years of unused room the way you can with a TFSA.

- Account lifespan: 15 years from when you open it

- If you never buy: Transfer the whole thing to your RRSP, tax free, without touching your RRSP contribution room

- If you do buy: Withdraw tax free. No repayment required, unlike the Home Buyers Plan through your RRSP.

The TFSA, by comparison:

- Annual limit: $7,000 in 2026

- Lifetime limit: None

- Carryforward: All unused room accumulates forever

- Account lifespan: No expiry

- Withdrawals: Tax free for any reason at any time

What To Actually Do

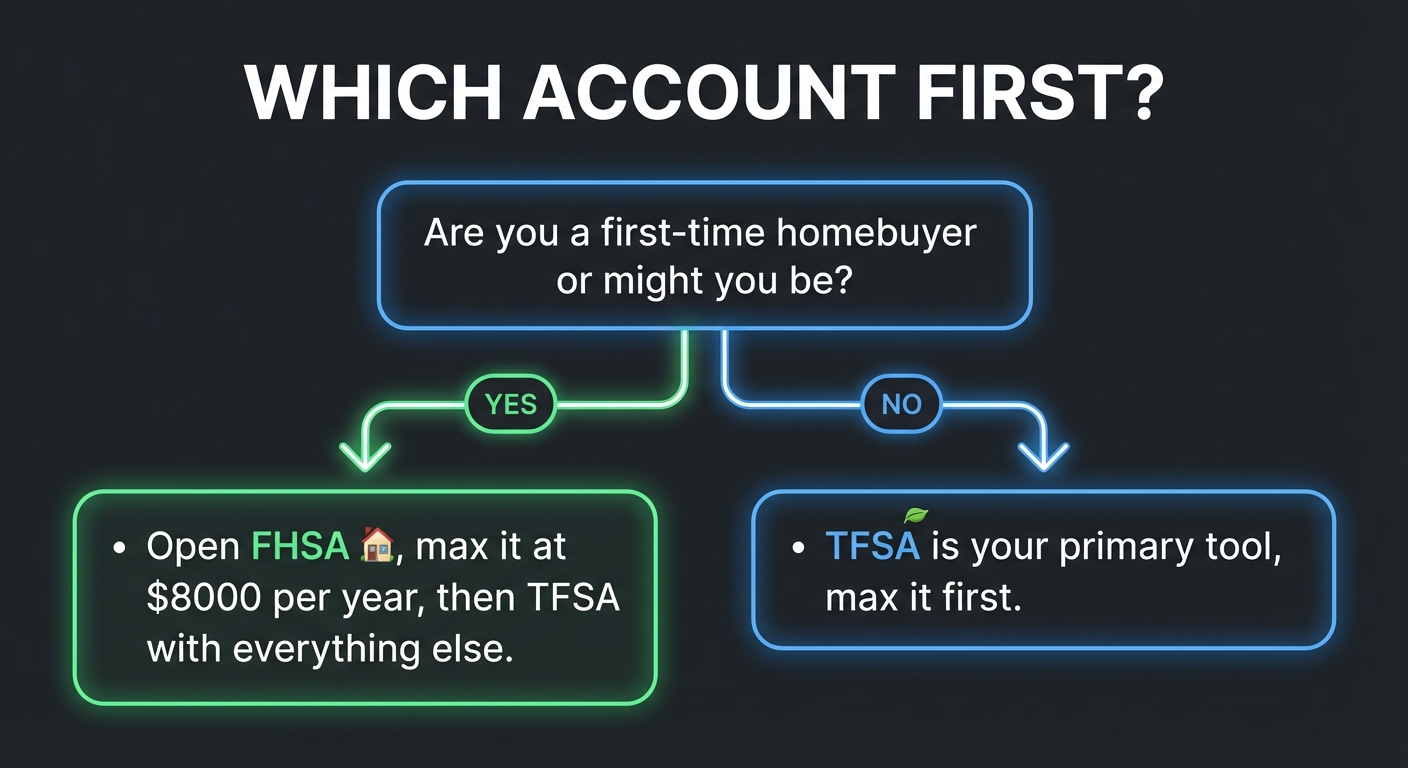

If you are a first time buyer or think you might be one day:

Open the FHSA first. Max it out before you add extra to your TFSA. You are leaving a free tax deduction on the table every year you do not.

The math is simple. If you are in the 20.5% federal bracket and you contribute $8,000 to your FHSA, you get $1,640 back on your taxes. Your TFSA would give you zero for the same contribution.

Do not wait until you are serious about buying. The 15 year clock starts the moment you open the account, not the moment you get serious. Open it now. Even if you contribute nothing for a year or two, your clock is running and you have the option.

If you are not a first time buyer or do not qualify for an FHSA:

TFSA is your primary tool. Max it before you do anything else. It is flexible, permanent, and lets you invest in whatever you want with no strings attached.

If you qualify for both and are thinking about a home purchase:

Max your FHSA first ($8,000), then direct everything else to your TFSA. You keep the flexibility of the TFSA while also getting the deduction the FHSA provides.

One thing worth knowing: you can use the FHSA and the Home Buyers' Plan together on the same purchase. The HBP lets you withdraw up to $35,000 from your RRSP toward a first home and that portion needs to be repaid over 15 years. The FHSA withdrawal does not. Stacking both on the same transaction is fully legal and genuinely useful if you have been contributing to an RRSP for a while.

The one thing people get wrong:

They think "I might not buy, so I'll skip the FHSA." This is backwards. If you open an FHSA, contribute for five years, and then decide homeownership is not for you, you roll every dollar (contributions, growth, all of it) directly into your RRSP. No tax. No penalty. No impact on your existing RRSP room.

You do not lose. You get the deduction, the tax free growth, and then a fat RRSP boost. The only scenario where the FHSA hurts you is if you never open one.

If you are eligible for an FHSA and you do not have one, you are paying taxes you do not have to pay. That is a choice, but it is not a smart one.

Free guide

Get the TFSA vs RRSP vs FHSA decision guide.

Join for practical Canadian investing guides, calculators, and plain-English account strategy updates. No spam, unsubscribe any time.