What to Do With Your Tax Refund in Canada (2026 Guide)

The average Canadian tax refund for the 2025 tax year is running around $2,000 per filer, according to CRA processing data from the 2026 filing season. For users of paid tax software, that number tends to run higher.

That is real money. Not life-changing on its own, but absolutely capable of moving the needle on your finances if you use it right.

The problem is that most people treat a tax refund like found money. They spend it on something they have been putting off. A weekend trip. New furniture. A laptop that was on sale.

This article is about what to actually do with it instead.

First: A Refund Is Not a Bonus

Before we get into strategy, this is worth saying out loud: a tax refund means the CRA was holding your money all year and giving you nothing for it.

You overpaid your taxes throughout the year via payroll deductions or installments. They held it. They paid you zero interest. You got it back in the spring and felt good about it.

That is not a win. That is a 0% loan you gave the government.

If you consistently get large refunds every year, consider adjusting your TD1 forms with your employer to reduce the amount withheld at source. That way you keep more of your paycheque throughout the year and can put it to work immediately.

But once the refund is in your account, the question is the same: what now?

Step 1: Kill the High-Interest Debt First

If you are carrying a credit card balance, stop reading and go pay it off.

Canadian credit cards charge 20 to 24 percent interest, and some go as high as 30 percent. There is no investment on earth that reliably returns 20 percent after tax. Paying off that debt is literally the best financial move available to you right now.

The average Canadian credit card balance sits around $3,929. If your refund covers that, or even a chunk of it, you just earned yourself a guaranteed 20 percent return. No brokerage needed.

The same logic applies to buy-now-pay-later debt, personal loans, and any line of credit charging more than around 8 to 10 percent. Pay it down first. The math is undeniable.

Step 2: Top Up Your Emergency Fund

Once the high-interest debt is gone (or if you never had any), the next move is making sure you have 3 to 6 months of expenses sitting somewhere accessible.

This is not glamorous. It does not show up as a line on your investment portfolio. But the emergency fund is what keeps you from going back into credit card debt the next time your car breaks down or you have a slow month at work.

Park it in a high-interest savings account (HISA). EQ Bank currently offers around 2.75 percent on everyday savings accounts. That is not exciting, but it is liquid and it beats letting cash sit in a Big 5 chequing account earning nothing.

Keep it boring. Keep it accessible. Keep it separate from your spending account so you are not tempted to dip into it.

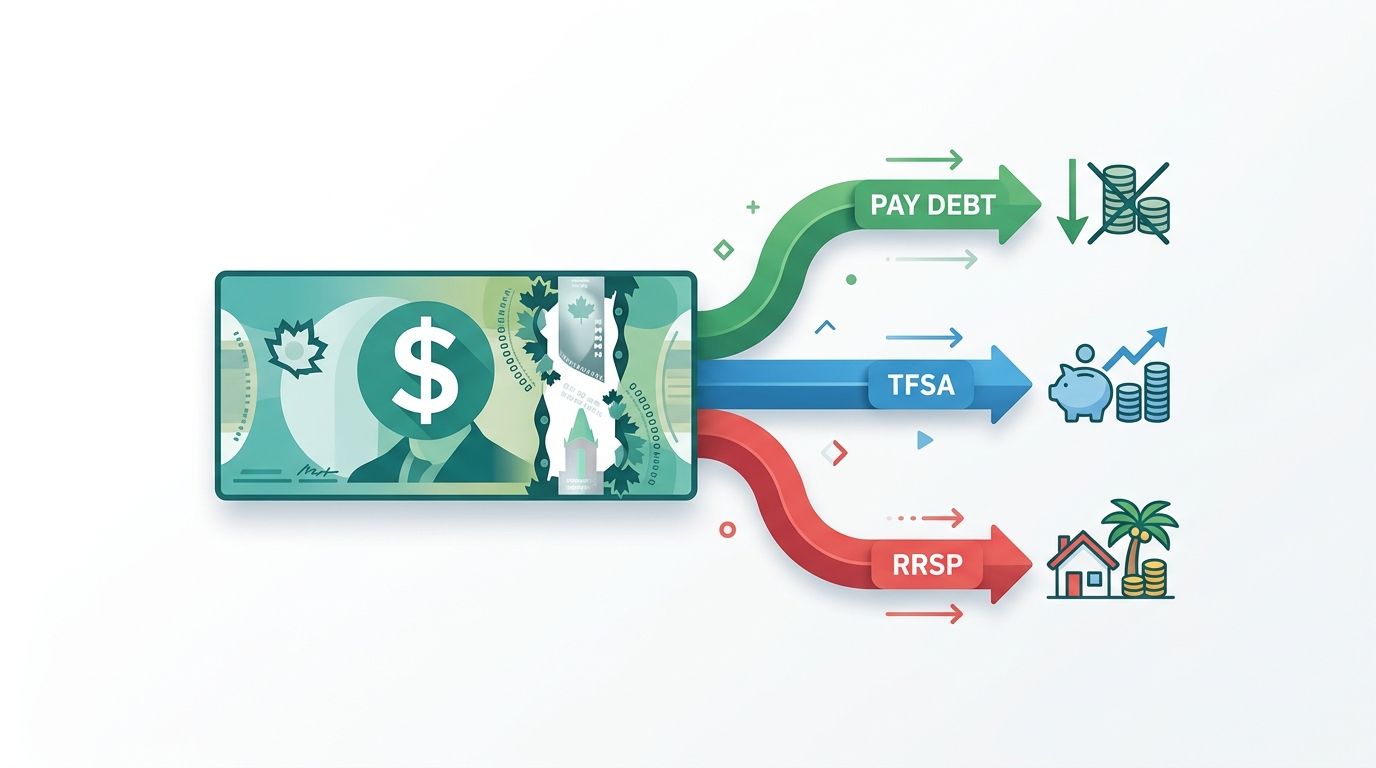

Step 3: Put the Rest Into Registered Accounts

Once the emergency fund is solid and the high-interest debt is gone, you are ready to invest.

Here is where things get interesting. You have three registered accounts to consider: TFSA, RRSP, and FHSA.

TFSA: The Default Answer for Most People

The TFSA is where most Canadians should start.

Your contributions grow completely tax-free. You can withdraw at any time for any reason without a tax hit. The 2026 contribution limit is $7,000, and if you have never contributed, your cumulative room could be as high as $109,000.

A tax refund going into a TFSA and into a broad market ETF like XEQT or VEQT is about as good as it gets for most people under 40.

There is no tax deduction when you contribute. But there is also no tax bill when you take the money out. That matters more over a long time horizon.

RRSP: Better If Your Income Is Higher

If you earn $60,000 or more per year, your RRSP becomes more attractive.

Every dollar you contribute reduces your taxable income. Contribute $3,000 to your RRSP and you reduce your taxable income by $3,000, saving you real money at your marginal rate. For someone in the 33 percent federal bracket, that is roughly $1,000 back from the government on top of whatever refund you already got.

The classic strategy is to take your RRSP refund and roll it right back into the same RRSP. You contribute, you get a refund, you contribute the refund, you get another smaller refund. Keep doing this and you compound your tax savings on top of your investment growth.

There are rules: you cannot access RRSP funds without a tax hit unless you are using the Home Buyers' Plan or the Lifelong Learning Plan. So it is less flexible than the TFSA. But the upfront tax deduction can be worth it depending on your situation.

FHSA: If You Are Planning to Buy a Home

If you are a first-time home buyer (or have not owned a home in the last four years), the FHSA is worth serious attention.

It gives you both the RRSP benefit (tax deduction on contributions) and the TFSA benefit (tax-free withdrawals when used for a qualifying home purchase). It is the only account in Canada that does both.

The annual contribution limit is $8,000, with a lifetime limit of $40,000. Open the account even if you cannot max it out right away. Contribution room accumulates from the year you open the account, not from the year you were born like the TFSA.

A tax refund of even $2,000 into an FHSA is $2,000 working for you tax-free until you need it for a down payment.

The Decision Flowchart

Not sure where to start? Use this order:

- High-interest debt (above 8 percent): pay it off first

- Emergency fund (3 to 6 months of expenses): top it up

FHSA: if you are planning to buy a home in the next decade — here is how it compares to the TFSA

- RRSP: if your income is above $60,000 and you want the upfront deduction

- TFSA: for everyone, always, especially if you want flexibility

You do not have to pick just one. If your refund is $3,000, you might put $1,500 into your TFSA and $1,500 toward a credit card balance. That is fine. The important thing is that the money goes somewhere intentional.

What Most People Actually Do

Surveys consistently show that the top uses of tax refunds in Canada are:

- Paying off debt (good)

- Saving (good)

- Day-to-day expenses (neutral, especially if you were tight that month)

- A big purchase or vacation (often a mistake)

The vacation answer is the one that stings. Not because treating yourself is wrong. Because the vacation usually goes on a credit card anyway, which means you paid off credit card debt with your refund and then immediately built new credit card debt for the trip. Net result: zero.

If you want to spend some of the refund on something enjoyable, that is a reasonable human decision. Just do it deliberately. Set a small percentage aside for that. Put the rest to work.

The Bottom Line

A $2,295 refund invested in a TFSA in a diversified ETF today, left alone for 25 years at a 7 percent average annual return, becomes roughly $12,400. Tax-free.

That same $2,295 spent on a weekend in Montreal is a weekend in Montreal.

Both are valid choices. But most people do not even realize they are making a choice. They just spend the refund and then wonder why they never seem to get ahead.

You know the difference now. Use it.

Keep reading

Useful next steps

XEQT vs VFV: Which ETF Should Canadians Buy in 2026?

XEQT vs VFV for Canadian investors in 2026. Which ETF belongs in your TFSA or RRSP, how they differ, and the simple answer for long term investors.

Read nextTFSA Maxed Out? Here Is What To Do Next

Once your TFSA is maxed, your next move depends first on your tax bracket, then your home plans, FHSA eligibility, RRSP room, pension, and taxable account needs.

Read nextInvestingInvesting Is Not as Scary as It Feels

Investing feels scary at first, but beginners do not need predictions, charts, or perfect timing. They need diversification, consistency, and time.

Read nextNewsletter

Get new posts in your inbox.

Finance and tech insights for Canadians — no spam, unsubscribe any time.