2026 RRSP Contribution Limit: What You Need to Know

The 2026 RRSP dollar limit is $33,810.

That's the maximum any Canadian can contribute to their RRSP in 2026, assuming they have enough contribution room. It's up from $32,490 in 2025, an increase of $1,320.

But here's the thing most people miss: the dollar limit is almost never the number that matters for you. Your actual contribution room depends on your income, your pension situation, and how much unused room you've been carrying forward.

What the 2026 RRSP Limit Actually Means

The $33,810 limit is a ceiling. You can contribute up to 18% of your previous year's earned income, to a maximum of $33,810.

So if you earned $100,000 in 2025, your new 2026 RRSP room is $18,000, not $33,810. To hit the full dollar limit you'd need to earn at least $187,833.

Most Canadians never actually contribute the maximum. What matters more is understanding your personal room and making sure you use it.

How RRSP Room Works

Your available contribution room has three components.

New room for 2026: 18% of your 2025 earned income, up to $33,810. This gets added to your room on January 1, 2026.

Carry-forward room: Any unused RRSP room from previous years accumulates indefinitely. If you've never maxed your RRSP, you likely have more room than you think. The CRA tracks this for you.

Pension adjustment: If you're in a defined benefit or defined contribution pension at work, your pension adjustment reduces your RRSP room. This prevents people with employer pensions from double-dipping on tax shelters.

Your exact room is on your most recent Notice of Assessment from the CRA. You can also log into CRA My Account to see it in real time.

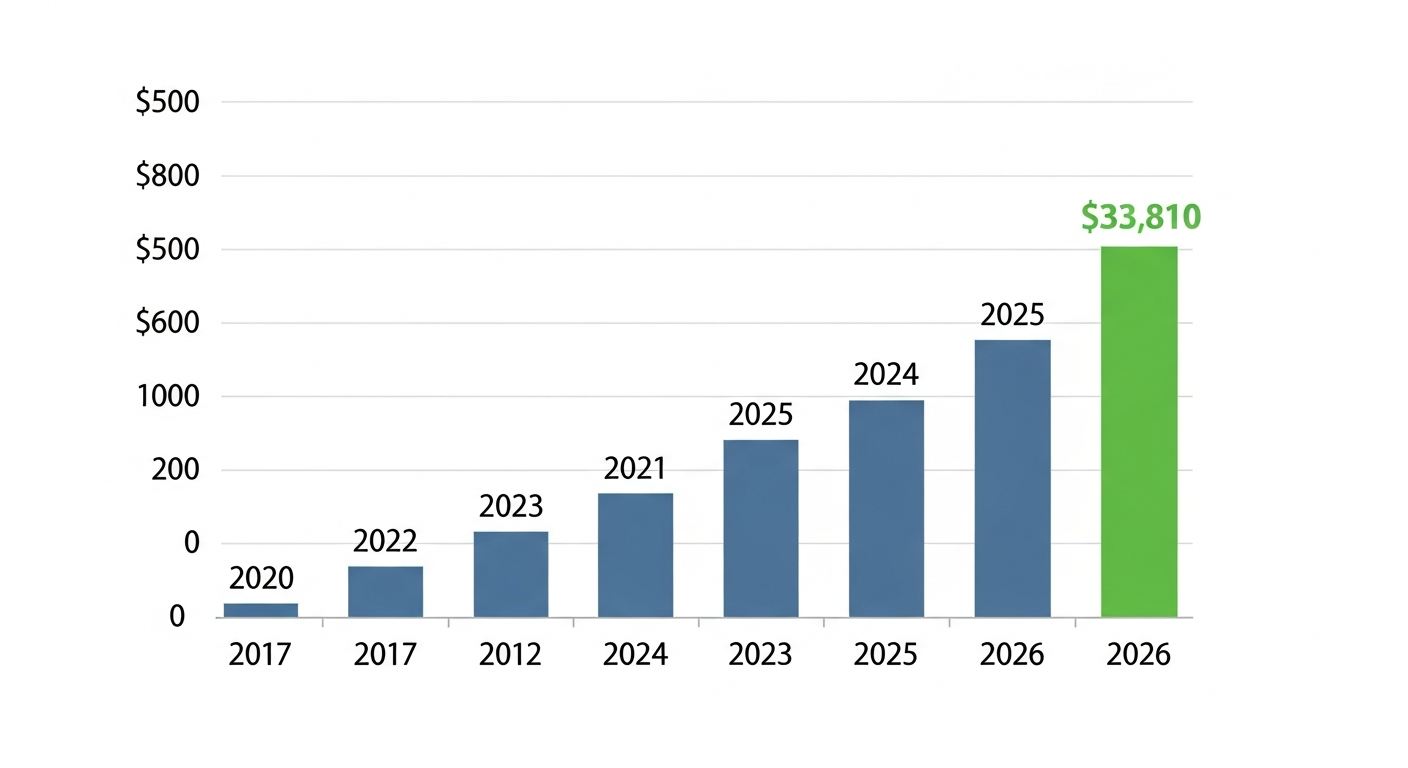

RRSP Contribution Limits by Year

Here's how the annual dollar limit has changed over the last decade:

2017: $26,010 | 2018: $26,230 | 2019: $26,500 | 2020: $27,230 | 2021: $27,830 | 2022: $29,210 | 2023: $30,780 | 2024: $31,560 | 2025: $32,490 | 2026: $33,810

The limit is indexed to the average wage in Canada. As wages rise, the limit rises with it.

The 2026 RRSP Deadline

Contributions made between March 3, 2025 and March 2, 2026 can be claimed on your 2025 tax return.

If you missed the deadline, any new contributions you make now count toward your 2026 tax year and will be deducted on your 2026 return.

The deadline always falls in the first 60 days of the calendar year, usually March 1 or 2.

Should You Maximize Your RRSP This Year?

The RRSP is a powerful tool but it's not always the right move to max it out. A few things to think about:

RRSP is best when your income is high now and will be lower in retirement. The tax deduction is worth more to someone in a 40% marginal rate than someone in a 20% rate.

If you're saving for a first home, the FHSA might come first. The First Home Savings Account gives you both a tax deduction and tax-free growth, same as the RRSP, but you can also withdraw it tax-free for a home purchase. For first-time buyers, that's a better deal.

If you're in a lower income year, filling your TFSA first might make more sense. Read our breakdown of RRSP vs TFSA: which do you fill first to figure out your best move.

The right answer depends on your specific situation. Our RRSP tax optimizer can help you figure out where the highest-value contribution dollars are for your income level.

How to Check Your Exact RRSP Room

Three ways:

Notice of Assessment: the CRA sends this after you file your taxes. Your available RRSP deduction limit is printed on it.

CRA My Account: log in at canada.ca and it shows your current room updated in real time.

Our RRSP Room Calculator: enter your income and carry-forward details and it calculates your exact room for 2026, including pension adjustment.

The $2,000 Buffer

The CRA allows a lifetime over-contribution of up to $2,000 without penalty. This is a buffer, not a bonus. Any amount above your room plus this buffer gets hit with a 1% per month penalty tax until you withdraw it.

Don't intentionally over-contribute. The buffer exists for accidental over-contributions, not as a strategy.

Quick Summary

The 2026 RRSP contribution limit is $33,810, up from $32,490 in 2025. Your personal room is 18% of your 2025 earned income up to that cap, plus any unused room from prior years, minus any pension adjustment. The deadline to contribute for the 2025 tax year was March 2, 2026. New contributions now count toward 2026.

Use the RRSP Room Calculator to find your exact number, and the RRSP Tax Optimizer to find the contribution that gives you the most tax savings.

Free guide

Get the TFSA vs RRSP vs FHSA decision guide.

Join for practical Canadian investing guides, calculators, and plain-English account strategy updates. No spam, unsubscribe any time.