Capital Gains Tax in Canada: What Every Investor Needs to Know (2026 Guide)

You sold some stocks. Your ETF grew. You sold a rental property you have been holding for seven years. Congratulations. Now the CRA wants to talk.

Capital gains tax is one of those topics that sounds complicated but is actually straightforward once you understand how the inclusion rate works. Most Canadians overpay, underpay, or just ignore it until tax season when their accountant delivers the bad news.

This guide breaks it down from the beginning.

What Is a Capital Gain?

A capital gain happens when you sell an asset for more than you paid for it.

You bought 100 shares of an ETF at $40 each. You sold them at $65 each. Your capital gain is $25 per share, or $2,500 total.

That gain is taxable in Canada. But not all of it.

Capital gains tax applies to:

- Stocks, ETFs, and mutual funds held in non-registered accounts

- Real estate that is not your principal residence

- Rental properties

- Cottages and vacation properties

- Cryptocurrency

- Business assets

- Collectibles, art, and precious metals

Capital gains tax does not apply to:

- Your principal residence (when you sell the home you live in)

- Investments inside a TFSA

- Investments inside an RRSP or RRIF (tax is deferred, not eliminated)

- Investments inside an FHSA when withdrawn for a qualifying home purchase

The Inclusion Rate: The Number That Actually Matters

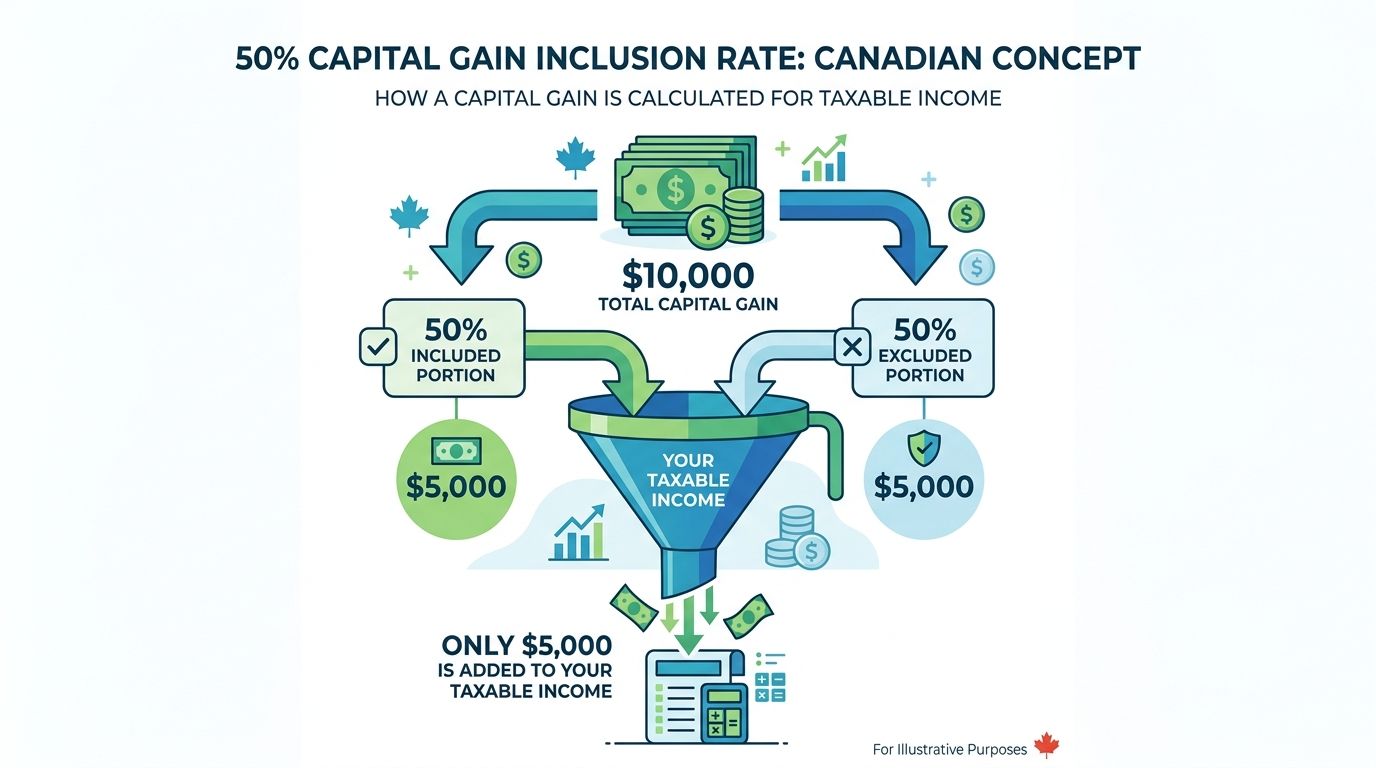

Canada does not tax your full capital gain. It only taxes a portion of it, called the inclusion rate.

In 2026, the inclusion rate for individuals is 50 percent.

That means if you have a $10,000 capital gain, only $5,000 gets added to your taxable income for the year. You then pay tax on that $5,000 at your regular marginal rate.

Here is what that looks like in practice.

Say you earn $80,000 in employment income in Ontario and you also realize a $10,000 capital gain by selling some ETFs in your non-registered account.

- Capital gain: $10,000

- Inclusion rate: 50 percent

- Taxable portion added to your income: $5,000

- Your new total taxable income: $85,000

- Effective combined marginal rate on the $5,000 (Ontario, ~$80K income bracket): roughly 43.41 percent

- Tax owed on the capital gain: approximately $2,170

So on a $10,000 gain, you pay about $2,170 in tax. The effective rate on the total gain is around 21.7 percent. That is much less than it would be on regular employment income.

This is by design. Capital gains receive preferential tax treatment compared to salary, and that is a meaningful advantage for investors.

What Happened to the Two-Thirds Increase?

You may have heard about a proposed change to the inclusion rate.

In the 2024 federal budget, the Liberal government proposed increasing the inclusion rate from 50 percent to 66.67 percent for capital gains above $250,000 per individual (and on all capital gains realized by corporations). The idea was deferred, debated, and then cancelled entirely.

On March 21, 2025, Prime Minister Mark Carney officially cancelled the proposed inclusion rate hike. As a result, the 50 percent inclusion rate remains in place for all individuals in 2026, regardless of how large your capital gains are.

This matters because there was a lot of confusion throughout 2024 and 2025 about whether to accelerate the realization of gains before a deadline. The answer is clear now: no change happened, and the 50 percent rate applies across the board for individuals.

Capital Gains by Province: It Varies

Because capital gains are added to your regular income and taxed at your marginal rate, the actual tax you pay depends heavily on your province of residence and total income.

Here are rough examples of the effective capital gains tax rate (what you actually pay as a percentage of the total gain) for someone earning $100,000 in employment income, realizing a $20,000 capital gain:

- Ontario: approximately 26.8 percent of the gain

- British Columbia: approximately 26.5 percent

- Alberta: approximately 24.0 percent

- Quebec: approximately 26.7 percent

These numbers shift as your income changes. The higher your income, the higher your marginal rate, and therefore the more capital gains tax you pay on the taxable 50 percent.

The key insight: capital gains are still taxed at lower effective rates than regular income, which is why investors who build wealth outside registered accounts are incentivized to hold for growth rather than earn salary.

When Do You Actually Owe Capital Gains Tax?

Capital gains tax is triggered by a disposition. That means:

- Selling shares in a non-registered account

- Converting one mutual fund to another (even within the same fund family)

- Gifting appreciated property to someone (including a spouse in certain situations)

- Transferring assets out of your estate upon death (deemed disposition)

- Switching between currency-hedged and non-hedged versions of the same ETF

Capital gains tax is not triggered by:

- An investment going up in value while you still hold it (unrealized gains)

- Selling within your TFSA, RRSP, RRIF, or FHSA

- Receiving dividends or distributions (those are taxed differently)

- Selling your principal residence (covered by the principal residence exemption)

The most common mistake Canadians make is not tracking their adjusted cost base (ACB). Your ACB is what you paid for the investment, including transaction costs, and it is what determines your actual gain or loss when you sell. If you do not track it properly, you end up calculating your gain incorrectly and potentially overpaying or underpaying tax.

Capital Losses: The Silver Lining

Capital losses are the inverse of gains. If you sell an investment for less than you paid for it, you have a capital loss.

Capital losses can offset capital gains in the same tax year. If you have $8,000 in capital gains and $3,000 in capital losses, you only pay tax on $5,000 in gains.

Unused capital losses can be:

- Carried back up to three years to offset previous capital gains

- Carried forward indefinitely to offset future capital gains

This creates a useful strategy called tax-loss harvesting. If you hold an investment that has dropped significantly, you can sell it to realize the loss and use that loss to reduce your tax bill on other gains. You can then immediately repurchase a similar (but not identical) investment to maintain your market exposure.

One rule to watch: the superficial loss rule. If you sell an investment at a loss and repurchase the same (or identical) investment within 30 days before or after the sale, the CRA denies the loss. This is to prevent people from generating artificial losses with no real economic change.

How to Legally Pay Less Capital Gains Tax

Use Your Registered Accounts First

The most powerful tool is the one most Canadians already have access to. Investments inside a TFSA grow completely tax-free. There is no capital gains tax on any gains realized inside a TFSA.

If you are choosing between holding a growth ETF in your TFSA or your non-registered account, hold it in the TFSA. The longer you expect to hold it and the more it grows, the bigger the advantage.

The 2026 TFSA contribution limit is $7,000. If you have never contributed before, your cumulative room could be as high as $109,000.

If you are planning to buy a home, the FHSA is even more powerful than the TFSA for this purpose. Contributions are tax-deductible (like an RRSP), growth is tax-free, and withdrawals for a qualifying home purchase are completely tax-free too. It is the only account in Canada that gives you both the upfront deduction and the tax-free exit. Max it before your non-registered account.

Hold for the Long Term

Because capital gains are only taxed when you sell (realized gains), holding investments longer defers your tax bill. A stock that grows from $10,000 to $50,000 over 20 years does not trigger any tax until you sell it. That $40,000 gain has been compounding for you tax-deferred.

This is one of the structural advantages of a long-term buy-and-hold strategy over frequent trading.

Use the Principal Residence Exemption

If your main home has appreciated significantly, you can sell it completely tax-free as long as you designate it as your principal residence for the years you owned it. This is one of the most valuable tax shelters available to ordinary Canadians and requires no special registration.

Be aware: you can only designate one property as your principal residence per year. If you own a cottage and a home, only one of them gets the exemption for each year.

Donate Appreciated Securities Directly

If you are charitably inclined, donating appreciated stocks or ETFs directly to a registered charity eliminates the capital gains tax on those securities entirely and generates a charitable tax credit for the full market value.

Instead of selling the ETF, paying capital gains tax, and donating the after-tax proceeds, you donate the ETF itself. The charity receives the full value. You pay no capital gains tax. And you get the donation receipt.

For investors with large unrealized gains and charitable intent, this is one of the most tax-efficient moves available.

A Quick Note on Corporate-Held Investments

For business owners and incorporated professionals: the cancellation of the inclusion rate hike matters for individuals, but the situation for corporations is more nuanced. Historically, corporations have faced different rules around investment income, the small business deduction, and passive income thresholds.

If you hold significant investments inside a corporation, the interaction between capital gains, refundable dividend tax on hand (RDTOH), and the general rate income pool (GRIP) is complex enough that you should be working with a CPA who specializes in corporate tax. This article covers the individual investor case.

The Bottom Line

Capital gains tax in Canada is less punishing than most people fear once you understand how the inclusion rate works. You are only taxed on half your gain, and that half is taxed at your regular marginal rate, not some special punitive rate.

The 50 percent inclusion rate is staying. The proposed hike is dead. That means the rules you plan around today are stable.

What matters most:

- Max out your TFSA first so your growth investments stay tax-free

- Track your adjusted cost base carefully in non-registered accounts

- Use capital losses to offset gains in the same year or carry them forward

- If you are donating, donate appreciated securities directly

Capital gains tax is not something to fear. It is something to plan around.

Keep reading

Useful next steps

XEQT vs VFV: Which ETF Should Canadians Buy in 2026?

XEQT vs VFV for Canadian investors in 2026. Which ETF belongs in your TFSA or RRSP, how they differ, and the simple answer for long term investors.

Read nextTFSA Maxed Out? Here Is What To Do Next

Once your TFSA is maxed, your next move depends first on your tax bracket, then your home plans, FHSA eligibility, RRSP room, pension, and taxable account needs.

Read nextInvestingInvesting Is Not as Scary as It Feels

Investing feels scary at first, but beginners do not need predictions, charts, or perfect timing. They need diversification, consistency, and time.

Read nextNewsletter

Get new posts in your inbox.

Finance and tech insights for Canadians — no spam, unsubscribe any time.